In my class, the very first tax law I mention, on slide two of day one, is named “An Act for Granting to His Majesty Several Rates or Duties Upon Houses for Making Good the Deficiency of the Clipped Money”. It was passed in England in 1696. It is known as the window tax, and it was a tax based on the number of windows you had in your house. In class we focus on this window tax, and I rarely mention what the tax was to pay for, specifically, “making good the deficiency of the clipped money”. What is that?

Read More

President Biden released a budget on Monday that called for such things as increasing the corporate tax rate and taxing the accruals on capital gains of folks with more than $100 million in assets (the taxiverse has yet to converge on a catchy name for this tax). I am seeing many academic tax folks of all stripes, economists, lawyers, etc., weighing in, expressing their love, or hate, of these plans. At this point, mostly love. This is all well and good—in my view, society is better off if people who have very informed opinions weigh in with their opinion (as opposed to uninformed people weighing in, which also frequently happens). However...

Read More

The destination based cash flow tax, or, as it was loving referred to among the large circle of economists who loved it, the DBCFT, was, at least in the minds of it supporters, an amazing tax. But, we don’t have one. One reason, I have heard talked about among tax people, is simply because the marketing of the tax was bad—starting with the name. DBCFT does not roll off the tongue. It does not conjure up favorable images of who will pay, or not pay, the tax. It’s too technical—not named so the every-person can understand it. What we name taxes matters. I call this phenomena optical taxation, where we pick names for taxes that conjure up images that make the tax appealing (if we want to pass it), or, make it look bad (if we want to get rid of it). Why, why the discussion around tax names?

Read More

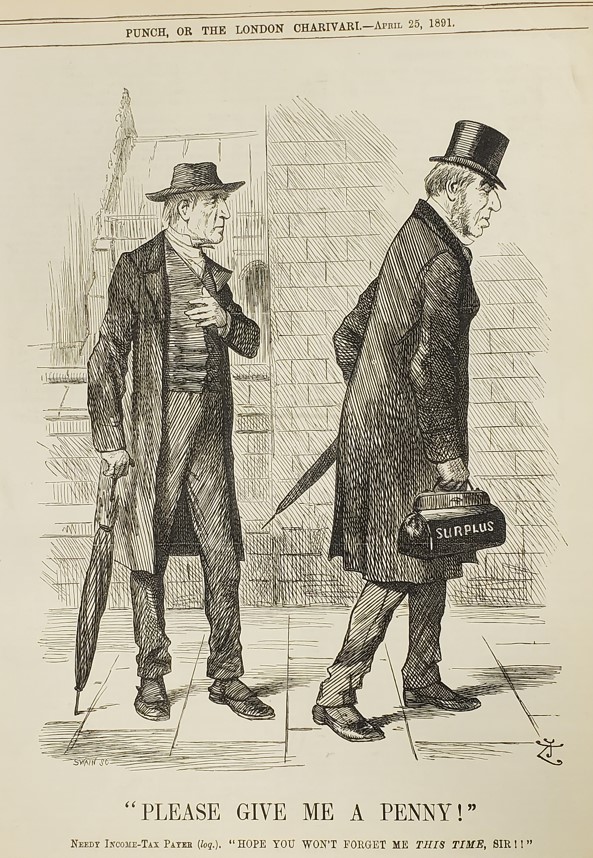

At the beginning of the pandemic, we thought state finances would be crushed. Then, as time progressed and we understood what the pandemic would do for sales taxes, that the federal government would be shoveling money to the states, etc., it became clear that many states would not struggle financially. And, indeed, some are mulling the possibility of cutting taxes to give back the extra money they have (and the problem that some federal aid seemed to preclude cutting taxes). I was reminded of this age old problem with what to do with government surpluses recently as I was reading the April 25, 1891 edition of Punch magazine, as one does, and saw this amazing poem, and, accompanying graphic:

Read More

Tax Notes, a key practitioner publication for tax professions, recently ran an article that was headlined “Is Inflation a Tax? Some Republicans Think So.” Is it only republicans that think inflation is a tax?

Read More

If you are a for profit company, or an individual, generally any income you receive, from any source, is taxable. The presumption is that everything you do is taxable. But, if you are non-profit, which is to say, you meet to requirements set forth by section 501 of the Internal Revenue Code to qualify and not have to pay taxes, then, you generally don't have to pay taxes on cash you bring in. For example, if you are a local soup kitchen and are a qualifying non-profit, and someone donates some money to help you buy soup, you don't pay taxes on that donation. But, what about the Girl Scouts? They are a non profit. But, they don't hand out soup for free-they sell cookies, and as far as cookies go, they are not cheap. Do they sell of those cookies tax free?

Read More

Martin Luther King Jr. has a lot to do with taxes, as does any interesting and important topic, person, event, or anything else. My first realization of the connection to Martin Luther King and taxes first occurred to me when The King Center, a center which focuses on helping understand Martin Luther King Jr., opened its digital archives. These archives had thousands of documents related to Martin Luther King Jr–letters he wrote, letters he received, speeches he gave, etc. While these digital archives have sadly been closed down since, when they were open, if you typed “tax” into the search bar, you got many, many results.

Read More

There have been recent proposals to tax the wealth, and income, of the extremely wealthy, which for whatever reason we have started calling billionaires. Many of these proposals have as a key feature the assurance that not many people will pay these taxes, because, after all, there are not that many billionaires. These taxes also come with the assurance that they will provide a lot of revenue, because, after all, billionaires have a lot of money. So, how many billionaires are there, and, how much are they worth?

Read More

Professor Reuven S. Avi-Yonah recently published an opinion in CNN Business.1 Here, I respectfully respond to several claims in that article. Claim: “Corporate America has perfected the art of dodging the taxes that everyone else pays.” Response: Sixty-one percent of individual taxpayers paid no federal income taxes in 2020. Even in non-pandemic years, this value is often in excess of 50 percent.2 There are more individual non-payers than corporate non-payers. Further, the loss from corporate tax evasion is much smaller than from individuals.

Read More

Bob Dole, Old Soldier and Stalwart of the Senate, Dies at 98. I just read this headline. And, the first thing that came to mind is that I have, as far as I know, the only digital version of Bob Dole's tax returns in existence in the digital version of The Tax Museum. When I was a PhD student at the University of Michigan, somehow I ran across news stories of Bob Dole releasing his tax returns as part of his campaign for president. But, Senator Dole ran for president before the wide-spread adoption of the internet, and, as a result, I could not find these documents online. I wrote a letter to the Robert and Elizabeth Dole Archives and Special Collections, and asked if they could send me the returns. They very kindly sent me a large packet of photocopies of the returns.

Read More

Accounting professors are pretty united in their opposition to taxing book income. But, accountants are not the only ones who have opinions in the academy about tax policy. Tax law professors often (more frequently than accountants, in my opinion) hold views on tax policy, and, I recently became very interested in what these views were on taxing book income. Some of these views are exceptionally well-informed (on many tax issues, more informed, in my opinion, than the opinions of accountants). With regards to the tax on book income, the only examples of tax law professors’ opinions on taxing book income came from a couple examples of very public support of taxing book income. In my mind, I imagined they all supported it. Do they?

Read More

Senator Warren has long pushed for a host of new taxes. Not just higher taxes, but new types of taxes unlike the ones in our current system. We and others have argued that some of these are notably bad ideas (see here, here, and here for examples). But, what is worse than a tax that is a bad idea? A tax that is a bad idea, motivated by half-truths and cherry-picked examples. Exhibit A is Senator Warren’s recently released report in support of taxing companies’ financial accounting income, entitled “Tax Dodgers: How Billionaire Corporations Avoid Paying Taxes and How to Fix It.” The report is frequently misleading and doesn’t in any way describe how corporations avoid paying taxes. The public deserves greater context and a deeper knowledge of the facts. The report is full of these examples—we will handle just the first three sentences of the report.

Read More

People often form strong, uninformed opinions on issues that actually require expertise to really understand. Tax policy is no different. One of the common laments about the Tax Cuts and Jobs Act (the TCJA--the Trump tax cut) in the academic tax circles in which I work was that it was all done behind closed doors, with little input from experts. In 1986 when the code was previously majorly overhauled, there were many hearings, testimonies, and more than a year of back and forth before the bill was passed. The TCJA was passed in a few short months, with little external expert input. Many in the tax community mourned the lack of dialogue about the TCJA. But, with all the handwringing about the lack of expert input about the issues back then, Democrats seemed bound and determined to repeat the experience again, pushing through an incredibly complex piece of legislation before it is well understood, or well vetted. The posterchild for this problem is the minimum tax on book income.

Read More

I have heard many interesting examples of nuances and complications of sales taxes/VAT, from the famous biscuit versus cake and Jaffa cakes controversy, to the fact that a sales tax in California hinged on whether animals in a zoo were edible and if they, in turn, were the ones consuming food, as opposed to either an edible animal or a human. But, this morning, someone sent me another amazing example. The VAT in the U.K. could depend, allegedly, on whether a gingerbread cookie is wearing pants.

Read More

There have been many recent proposals to tax the wealth of the very wealthy. Generally, our tax system only taxes income, so, it is hard to think about what it means to tax wealth. For example, a 4% wealth tax seems small compared to, say, a 37% income tax. 4% is way less than 37%! But, how do these numbers really compare? Luckily, there is a way to convert from one tax rate to another.

Read More

Michelle Hanlon and I recently sent a letter, cosigned with 264 fellow accounting and tax academics, expressing concern about including financial accounting in the tax base.

Read More

I was watching I Love Lucy last night, season 1, episode 35, named “Ricky Asks for a Raise”. The episode starts with Ricky getting tutored by Lucy on how to ask for a raise. After his training, the moment comes where he asks Mr. Littlefield, his boss, for a raise, and, we learn what is keeping him from higher pay. What?

Read More

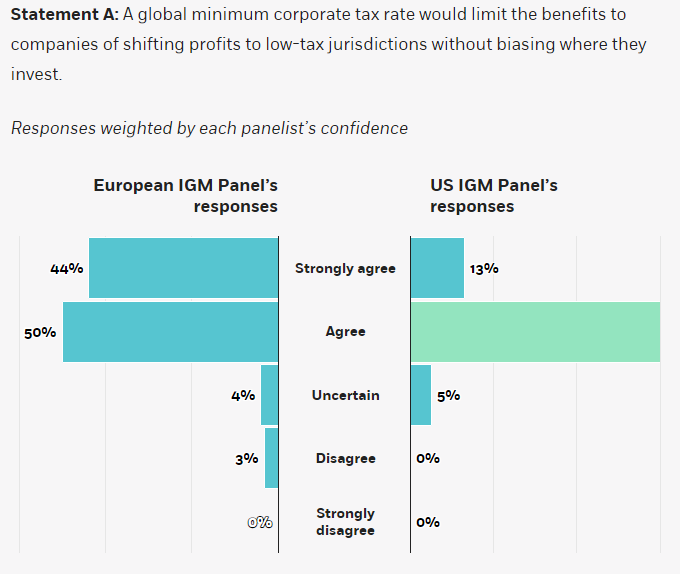

Generally, we think of a higher domestic tax rate discouraging domestic investment (subject to some caveats). One of the mechanisms through which investment is discouraged is companies simply move the investment they would have done in the country that is going to increase its tax rate, and, move it abroad. So what happens if a bunch of countries get together and form a corporate tax cartel, agreeing on a minimum tax rate? Will a global minimum tax rate reduce profit shifting without affecting investment?

Read More

I wrested in high school, and, have always had a little bit of a sore spot for what they call “wrestling” on TV—these people acting out some wrestling match, where chairs are thrown, stupid costumes are worn, and, the whole thing is pretty clearly a sham. You know what I am talking about—WWF, WrestleMania, Hulk Hogan, the piledriver, etc., etc., etc. Well, a long time back, World Wide Entertainment, one of the companies that is in charge of this type of fake wrestling, had to admit what it ran was a sham. All predetermined. Staged. Like an intricate ballet dance, but, smaller costumes, and larger bodies. Why? Taxes, of course.

Read More

Every year, individuals and companies pay taxes, based on the rules in the Internal Revenue Code. The Internal Revenue Code is the highest form of tax law in the United States, and is created by the United States Congress. For example, when Congress changes a tax law, what they are really doing is amending the Internal Revenue Code. So, what’s the purpose of the Internal Revenue Code?

Read More

North Carolina is currently considering reinstating a state Earned Income Tax Credit (EITC). There is a great deal of information and research on the federal EITC. Research has shown that it decreases welfare entries[i], encourages higher levels of education for the children of workers claiming EITC and increases economic mobility[ii], and encourages entry into the labor force[iii], and has a positive impact on infant and child health[iv]. Those are just examples of the positive impacts it has been found to have on low- and moderate-income households. In fact, it is estimated to have lifted 5.6 million people out of poverty in 2018 and 3 million of those were children.[v] If this was not enough reason for bipartisan support, the structure of the EITC also creates policy that many can unite behind. The EITC, at the federal level, is a refundable credit that encourages labor force participation by requiring recipients to be in the work force and increasing in generosity for low-income workers. Depending on the number of children in the household and the marital status of the taxpayer, the credit can be as high as $6,600 (married with 3 or more children). The credit eventually plateaus and then slowly decreases. Below is the structure in 2018. The current federal EITC is structured differently, and it is unclear whether the current structure will be permanent or not.[vi] Thus, the EITC provides important income supports for low- and moderate-income households, with a historic emphasis on those with dependent children, while also encourage labor force participation.

Read MoreThe news is often filled with bad stories, so how about a good one? We’ve already heard that there are big profitable corporations that pay no tax, but did you know that some companies generously share their profits with the government out of the goodness of their corporate hearts? Since 2017, when Congress lowered the statutory corporate tax rate to 21%, VF Corp. (the maker of brands such as North Face and Vans) had a domestic effective tax rate of 174%. In other words, it expensed 174% of pre-tax domestic profit in U.S. taxes. Cisco and Western Digital had effective tax rates of 67% and 236%, respectively. The corporate generosity posterchild, Merck, had a rate of 303%. Sensing our country’s deep budget problems, these companies dug deep and gave until it hurt. We should move them to the top of the world’s most admired companies.

Read More

I recently purchased a bag of ice, and, noticed on it a little emblem, “Ice is Food.” I wondered why the ice folks would want to assure me that ice is food. I thought about whether I thought of ice as food. Sometimes I use it to cool coolers, and, it does not get consumed internally. The bag I was buying was meant to cool drinking water, so, I was going to ingest it. So, sure, sometimes it is food. But, why are the ice people so anxious to convince me ice is food?

Read More

Americans are notoriously obese. Whenever I travel outside the country I am reminded of how fat, on average, my countrymates are (including me!). What is the problem with being fat? There are tons of problems, of course. Some of the problems derive from simply carrying around too much weight, unproductive mass that puts strain on knees, hips, etc. Fat is extra, unproductive person, clinging to you, dragging you down, making you slower, and, in general, slowing killing you. What does this have to do with taxes, or corporations, or, anything relevant to this blog?

Read More

Senate Democrats are considering an array of new taxes to pay for their large budget bill. One tax being considered imposes a 2 percent tax on corporate share repurchases. It has been a rough couple of years for share repurchases. They continue to take a beating from buyback bullies on both the right and the left. How frequently do Sen. Bernie Sanders (I-Vt.) and former President Trump agree? Buybacks are that rare instance.

Read More

AOC is only one of many politicians who have favored increasing the tax burden on the rich, as she most recently made headlines for in her tax the rich dress. In my class I always like to point out the tax dealings of those who favor higher taxes. I highlight Hillary Clinton’s shell Delaware corporations, John Kerry’s yacht tax avoidance, John Edwards and Joe Biden’s avoidance of self-employment taxes, etc. (I also point out the tax deeds of many who favor lower taxes, but, these are less entertaining, because these folks don’t want to increase taxes on other people). I always point out that these people are doing nothing wrong. All these strategies are ostensibly legal, and, as Learned Hand famously notes, “Any one may so arrange his affairs that his taxes shall be as low as possible; he is not bound to choose that pattern which will best pay the Treasury; there is not even a patriotic duty to increase one's taxes.” But, the dress affair is interesting in that it involves someone allegedly illegally evading taxes. Who?

Read More

Twice this week, I listened to someone mention the three jobs taxes are intended to do. One of these times was on Lisa De Simone and Bridget Stomberg’s excellent tax podcast, Taxes for the Masses, where they mentioned the canonical three jobs of taxes: 1. Raise revenue to run the government, 2. Redistribute income, and 3. Change taxpayer behavior. These three purposes of taxes are pretty standard, and, extremely useful for thinking about tax policy. I have mentioned them myself many times. But, I would like to propose that there is a fourth purpose of taxes that we should always keep in mind. What is it?

Read More

There has been a huge debate over share repurchases lately. The most recent tax proposals by the democrats includes a tax on share repurchases. Why all the repurchase hate? In my opinion, most of the repurchase hate stems from a misunderstanding of repurchases, what they do to share price, earnings, the nature of the company, etc. Many people who don’t like repurchase s simply either do not understand repurchases, or, chose to ignore what buy backs are. What is the alternative to a buyback? If a company wants to get rid of the cash and hand it back to shareholders, the alternative is to pay more in dividends. Increasing a regular dividend is a pretty large commitment, so, I think it is most appropriate to think about the alternative to a repurchase as a special dividend. And, there are big tax differences between a special dividend and a share repurchase.

Read More

Many people are frustrated with how much CEOs get paid. There have been many proposed solutions to this perceived problem. One that has gained traction recently is to impose some kind of tax on the difference between CEO pay, and, the average worker in the corporation’s pay. One proposal that has been around for a while, but, currently being floated by democrats, would have an incremental tax on the difference between average CEO pay and the median worker, up to a maximum of a 5% tax for companies that pay their CEO more than 500 times the average worker. There are so many interesting ways around this tax, some of which are intended by the proponent of this tax (pay employees more, or CEOs less), and some of which would be unintended (outsourcing more work, using more independent contractors, shifting income abroad if the extra tax applies only to domestic income, etc.). But, one way I have not heard discussed goes back to the time honored method of bunching, useful when taxes are imposed with maximum (or minimum) thresholds. Here is how it would work:

Read More

I recently emailed this to Representative Alexandria Ocasio-Cortez. Here’s to hoping… Representative Ocasio-Cortez, I am the chief curator of The Tax Museum, a collection of thousands of tax-related artifacts housed here at the University of North Carolina, Chapel Hill (examples of some of our items can be found at thetaxmuseum.org). I would like to inquire about your willingness to donate...

Read More

Milton Friedman famously defended the position that “the social responsibility of business is to increase its profits”. Let’s assume that Friedman was wrong, and that the social responsibility of business is not merely to increase its profits, and that it needs to consider the many stakeholders involved in business outcomes. Under the Friedman framework, with regards to taxes, firms should seek to maximize profits, which may involve paying as little in taxes as is legally possible (subject to the other costs of tax avoidance, and assuming the law is clear). Simple enough. But what about under the anti-Friedman framework? How Much Should Socially Responsible Firms Pay in Taxes?

Read More

There is a very interesting and useful paper on the design of tax returns that suggests that based on psychology research, we should redesign the tax return so that the location of the signature of the taxpayer is adjusted to elicit more honest behavior from the taxpayer. I was aware of this paper some time ago, and, have proposed a field experiment that would redesign the tax return for a state I was communicating with, but, institutional barriers didn’t allow what would have been a fascinating field experiment to happen. Luckily. Why luckily?

Read More

I am sometimes called by journalists or other organizations who want me to confirm their biases that some company is not paying enough in tax. The conversation never goes as the journalist wishes, starts to get real complicated, as I explain that the effective tax rate the journalist is looking at takes a lot of background to understand, and that a low rate is very often nothing nefarious. This is a pretty universal sentiment among accounting professors. Someone recently sent me a document written by Seymour Fiekowsky and issued by the Office of Tax Analysis at the U.S. Treasury Department that does an amazing job explaining this. Following is a long excerpt. But, before that long excerpt, it is fascinating to me what year this came out. 1977! 44 years ago! Amazing. The excerpt:

Read More

I am the curator of The Tax Museum, the largest collection of tax artifacts in southern Chapel Hill. This means that every once in a while, usually late at night, I just roam around the internet looking for interesting tax things on the internet, some of which could eventually be tied to physical items I could acquire for my collection. I recently ran across the website of the National War Tax Resistance Coordinating Committee, and, ordered some items from their store. These items were promptly and personally shipped, and I was delighted with these items. What is the National War Tax Resistance Coordinating Committee?

Read More

Tax folks, as a collective group, have a lot of pet peeves. One is attributing the tax law, or the Internal Revenue Code, to the Internal Revenue Service. Congress writes the tax law, and, the Internal Revenue Service enforces it. In a recent excellent podcast by Bridget Stomberg and Lisa De Simone, they remind us of this fact, and, reference a Texas politician who likes to refer to the Internal Revenue Code as the “IRS Code”. Who is this politician, and, is he so uneducated as to think that the good people at the IRS are the authors of the tax code?

Read More

President Biden has proposed a 15 percent corporate minimum tax. Has he forgotten that the U.S. already has a minimum tax rate and that it’s higher than 15 percent?

U.S. companies are obligated by law to pay, at a minimum, 21 percent of their U.S. taxable income in taxes, after adjusting for losses and tax credits. The 21 percent federal rate has been in place since 2018, and before that, the minimum tax rate was 35 percent. The minimum tax we have today is just the normal corporate income tax rate. So why all the talk of a new minimum tax if we already have one?

Read More

We keep hearing that the corporate tax code is riddled with “loopholes” and that large corporations are tax cheats for using them and not paying their “fair share.” Is it true? No, most large corporations pay the amount in taxes they do because Congress expressly wrote the tax code to allow them to pay that amount.

Read More

A few weeks ago, I testified before Congress. As part of this process, members of the Senate can send me written questions that I am to respond to for the written official record of the hearing. It is my understanding that these official records might be a year or two in coming out, so, in order to have someone see this Q&A before the zombie apocalypse, I am including a few of the more interesting questions, and my responses, here on this blog. Question 3. Some taxes have been passed by Congress on the basis that they would largely target the ultrawealthy and then have gradually been expanded to include a larger set of taxpayers. Can you comment on this history?

Read MoreProPublica posted, this morning, a report on the tax records of the super wealthy. Based on what seems has to be illegally obtained data, they report on the tax payments of Bezos, Musk, Buffet, et al. I will save you readings thousands of words of story by reminding you of a feature of our tax code: If you don’t sell a capital asset, like a stock, you don’t pay any taxes on the gain. The end. Like pretty much every other jurisdiction in the world, we believe in the principle of realization. So, if you are Bezos, Musk, or Buffet, no matter how much your stock is worth, if you don’t sell the stock, you don’t pay taxes on it. We already knew these folks paid basically nothing in taxes, as they don’t sell lot of stock, Berkshire, Amazon, and Tesla pay no dividends, and that would be what generated those tax payments. There is no story here, at least for anyone who knew this basic fact about the tax law. But, I imagine we will hear a lot more about this story, and others based on this likely-illegal data, in the future. Whether they should pay taxes is an entirely different point. But, our current tax system is not designed so that they do.

Read More

A few weeks ago, I testified before Congress. As part of this process, members of the Senate can send me written questions that I am to respond to for the written official record of the hearing. It is my understanding that these official records might be a year or two in coming out, so, in order to have someone see this Q&A before the zombie apocalypse, I am including a few of the more interesting questions, and my responses, here on this blog. Question 1: Estate taxes. Senate Majority Leader Schumer has stated, with regard to the estate tax “…any organic business--a farm, a small business, and frankly a large business--that would have to be broken up because of the extent of the tax should not be. A business is an ongoing organism. It employs sometimes 10 people and sometimes 10,000 people. To have to break that business up to pay any tax, to me, is counterproductive.” Do you agree that the tax code should not inhibit owners of any size business from being able to pass along that business, in full, to future generations?

Read More

I teach a class here at the Kenan-Flagler Business School at UNC where we discuss an employee negotiating how much they will get paid by their employer. My students invariably think the corporation will prevail and get the long end of the stick—these students come conditioned by society to believe that when the giant corporation and the puny employee face off in a compensation clash, a salary show-down, or a bonus brouhaha, the corporation has all the bargaining power, and, will be able to run roughshod over the powerless employee. That kind of thinking largely dictates how we regulate compensation. For example, we set a minimum wage, presumably because absent some government protection, giant firms would take advantage of their helpless employees. We have a whole host of regulations and laws that protect employees from employers because deep down, we seem to fundamentally believe that corporations will abuse their employees absent these laws. This thinking is especially prominent on the left side of the political aisle—protect weak and powerless employees from powerful employers. With one exception...

Read MoreCorporations are able to deduct some strange things on their tax returns. But new tax proposals from President Joe Biden and Sen. Elizabeth Warren introduce a few doozies. For example, if a company were to settle a sexual harassment lawsuit subject to a nondisclosure agreement, that would be tax-deductible. If a company were to illegally bribe foreign officials, that would be fully deductible, as would be the penalty from the Justice Department once it was caught. And if a company were found guilty by the Environmental Protection Agency (EPA) of illegally dumping nuclear waste near an elementary school, that, too, would be tax-deductible under the Biden and Warren tax proposals. Yet none of these deductions are allowed under our current tax system. Sound crazy? We think it does. But because Biden and Warren want to place a tax on financial accounting income (the income that companies report to investors), everything that is allowed as an expense for financial accounting purposes would become a proper deduction under the new proposed taxes. And that includes a lot of things.

Read More

Michael Jackson died on June 25, 2009. That was a long time ago. Just yesterday, the U.S. Tax Court determined that Michael Jackson’s image was worth $4.2 million. The IRS had initially asserted it was worth $161 million, but, now, nearly 12 years after Jackson’s death, the value has come in at a tiny fraction of that. What does this have to do with the wealth tax?

Read More

On Tuesday I testified before a Senate Subcommittee, chaired by Senator Warren, about our nation’s broken tax code. The week prior to the event, I prepared extensively for the event. I’ve been publically critical of Senator Warren’s hallmark corporate tax proposal, the Real Corporate Profits tax, so I went in expecting to be put through the wringer as she drilled me with hard questions. I sat at my computer, gave my opening statement, and then waited for Senator Warren to pounce. Sadly, my wait was protracted. Senator Warren did not ask me any questions. In fact, she didn’t ask any questions to witness she did not invite—and she had not invited me. While I was spared the hot seat, I was disappointed. Why? Because I felt like I had answers to some good questions Senator Warren should have asked. Answers that could help us have more constructive conversations about tax policy, and that move us past the political rhetoric. Here are two examples:

Read More

At a hearing last month, Senator Sanders asked why Amazon didn’t pay any taxes despite having huge profits. At least two people got a crack at the question. In my opinion, much was missed. So, what is correct the answer? It depends on how persnickety you want to be.

Read More

Danaos is a company that owns and leases large containerships. The giant kind of ship, like recently got wedged in the Suez Canal. But, this article is not about ship wedgies, but rather, what would happen with Danaos if we were to have a real corporate profits tax, as Elizabeth Warren proposed on the campaign trail, and, as she recently mentioned in a hearing last month. So, what are the issues with Danaos and the real corporate profits tax? Here are some examples:

Read More

It’s been a rough year to be the owner a magical kingdom. I have a friend who once worked security for Disney, and, he said the guards were employed for several months in 2020 keeping people out of the park—not a big money making venture. Disney went from a $10.9 billion dollar pre-tax profit in 2019, to a $2.4 billion dollar loss. Elizabeth Warren would like to tax book profits, in what she calls her Real Corporate Profits Tax (it turns out, I suppose, we have been heretofore taxing fake profits). While this plan has not been talked about as much recently, Senator Warren recently mentioned it in a hearing last month. So, what do you do with a firm like Disney?

Read More

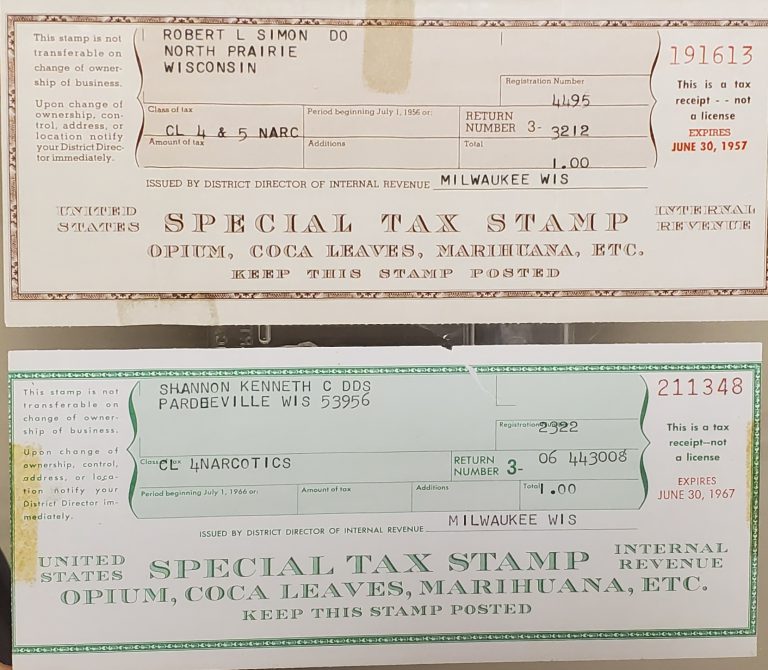

Taxes and marijuana have a long and interesting history. Currently, weed is legal at the state level some places, but, at the federal level no where. This causes businesses selling ganja a lot of trouble, as, for example, banking regulations prohibit banks for dealing with businesses involved in selling illegal goods (which grass currently is). The unbankedness, at least historically, of vendors of dope lead to the fascinating result that these businesses had to pay their taxes in cash, which for a large business can be a lot of cash. One of the most remarkable interactions between mary jane and taxes is that taxes have frequently been used as a justification of the legalization of the reefer--pot proponents taut the extra tax inflows that will result from taxed sales of the wacky tobaccy. In any event, on 4/20, those who are into this sort of thing celebrate the locoweed. So, in honor of them, here is an artifact from The Tax Museum. It is a part of tax stamps sold associated with the use of "Opium, coco leaves, marihuana, etc.", by two Wisconsin dentists in 1957, and, 1967. This stamp was donated to the The Tax Museum by its most generous benefactor.

Read More

In the last couple weeks, things have been getting much more specific about President Biden’s plans to increase corporate taxes, and his plans have got a lot of media air time. Further, signs are suggesting the tax hikes will be legislatively possible to do pass. For example, on Monday, the Senate Parliamentarian concluded that reconciliation can be used more than once this year, meaning that if a majority in the House and Senate can agree on a tax bill, it can become law. The proposed hikes are not minor tax adjustments. The corporate rate increase would be meaningful, the tax on foreign income would be substantial, and, the tax on book income would lay the hurt down on some of the biggest corporations on earth. But yet, as one of my accounting colleagues here at UNC recently noted, we have not seen a large drop in the stock market that seems attributable to taxes. What gives?

Read More

Joe Biden and the Democrats want to change how multinational firms pay taxes. They argue that the current tax system enacted as part of the Tax Cuts & Jobs Act (TCJA) of 2017 encourages profit-shifting. Thus, the Biden Administration and the Department of Treasury are proposing a new global minimum tax and the repeal of the Base Erosion and Anti-Abuse Tax (BEAT). They suggest this because they think the BEAT is not working because companies can just plan around it, and not pay it. So, is there evidence that such planning actually occurs?

Read MoreMany are calling for increased funding at the IRS. But, how much is appropriate? I don’t know the answer. But, one thing comes to mind—let’s just try something, and, see what happens. Congress (at least some version of Congress, i.e. a republican controlled Congress) knows it has the political will to cut the IRS budget (unlike budgets of other government organizations). And, unlike other parts of the government, the IRS has pretty measurable outcomes. If we cut defense spending and we don’t get invaded by a hostile government because they are afraid of our military, we don’t really know if the cut hurt the effectiveness of the military. But, the IRS has a mission that can pretty easily be measured, in dollars collected. Let’s increase their budget for 3 years, and see what happens. So, how much extra?

Read More

At a recent hearing of the Senate Budget Committee styled “Ending a Rigged Tax Code,” Chairman Bernie Sanders opened proceedings with a list of familiar economic “absurdities” and “obscenities,” as he called them, stating among other things that Jeff Bezos and Elon Musk alone own as much wealth as the poorest 40% of Americans combined. There was one new obscenity for the list: the claim that the wealthiest 1% of Americans are evading about 20% of their tax obligation, amounting to hundreds of billions annually. This figure comes from a recently published paper by economists John Guyton, Patrick Langetieg, Daniel Reck, Max Risch, and Gabriel Zucman. Zucman in particular has been a prominent voice in academic discussions around the precise scale of various measures of income and wealth inequality, most notably with his UC Berkeley colleague Emmanuel Saez, and Zucman was on hand to testify before the Committee.

Read More

A recent paper by John Guyton, Patrick Langetieg, Daniel Reck, Max Risch, and Gabriel Zucman finds that previous IRS estimates of income misreporting at the top of the individual income distribution are understated. By a lot. In other words, the paper finds that rich people cheat on their taxes much more than we used to think. Random audits, which are used to detect this cheating, are less accurate for rich people than poor people, as the rich are able to use tax evasion techniques that are particularly difficult to find upon audit (holding asserts in difficult-to-discover entities in countries with low disclosure). I thought this was an interesting and useful paper. I won’t dive into any details here. But, as someone who thinks a lot about corporate income, given this paper, the question becomes, how should I think about IRS estimates of non-compliance for large corporations?

Read More

In classes I teach, at least once a semester, an issue will come up where I will ask the question, “when was the last time you heard of a government bureaucracy saying it is well-funded, and needs no more money?” The answer I share, and, that my students reply with before I share, is “basically never.” This is not only true of government organizations, but, basically every organization—all think they are underfunded, could use more money, etc. With this in mind, I hear the increasingly frequent claims that the IRS is underfunded. It is true that the marginal revenue produced by a marginal dollar into the IRS budget is much more than one, and, given that fact, if the IRS were a business, we should keep investing in it. But, the IRS is not a business. While it is true we should not think about investing in the IRS as we thinking about investing in a business, in my opinion, we should likely increase funding to the IRS. Why?

Read More

For many years, the US corporate statutory tax rate was the highest among developed nations, at 35%. In 2017, Congress passed the Tax Cuts and Jobs Act, which lowered the corporate statutory tax rate to 21%. While that seems like a big decrease, even at 21%, combined with state taxes, the corporate statutory tax rate was still in the middle of the pack when compared to other developed nations. We had achieved a goldilocks level of tax—not too high, not too low, rather, right in the middle of all the other countries we compete with. President Biden is now proposing to raise the tax rate to 28%, which, when combined with the state taxes that companies in the U.S. face, will put us back at the top again—the highest corporate statutory tax rate. Is that a bad thing?

Read More

Yesterday Biden unveiled his infrastructure plan, which is funded in part by an increase in the corporate tax rate from 21% to 28%. Relative to the pre-TCJA 35% top marginal corporate tax rate, or even the current 37% top individual marginal tax rate, this may not seem like a bitter pill to swallow. But consider a couple of facts that I was reminded of by Rohit Kumar (Co-leader of PwC’s Washington National Tax Services) during our February 10 CPE webcast, and Manal Corwin (Principal in Charge of KPMG’s Washington National Tax Office), during our March 26 UNC tax symposium:

Read More

When you ask tax directors why they don’t do more tax planning, one common response is that they don’t want to damage the reputation of their company—they don’t want to end up on the front page of the Wall Street Journal and make their company look bad. But, when was the last time you read a story of a tax planning firm, and, decided not to buy something? If you are like most people—never. In a recent paper, coauthored with Scott Asay, Jake Thornock, and Jaron Wilde, we dig deep into the concept of a tax boycott. Many people remember when Starbucks in the UK was boycotted because of their taxes. But, how common is that, really? And, even with Starbucks specifically, was it actually meaningful?

Read More

Last week the Senate Finance Committee held a hearing on How U.S. International Tax Policy Impacts American Workers, Jobs, and Investment. There was some (disingenuous) discussion of taxing book income, at about 1:42:00. The eminent Fabio Gaertner and I decided to write an official statement for the record about including financial accounting income income in the tax base, and, submitted it as part of the official record associated with the hearing. Following is our full statement:

Read More

Taxes are fascinating things. They have changed history, shaped society, and, continue to be one of the biggest tools policymakers use to meet their objectives. Taxes have changed, shaped, and are tools because they change behavior—people work differently, consume differently, dress differently, eat differently, breed differently, etc., because of the taxes imposed on them. I love hearing examples of interesting situations where the intersection of taxes and incentives meet, and the often unintended consequence of this intersection. Which is why I loved the new book, Rebellion, Rascals, and Revenue: Tax Follies and Wisdom through the Ages by Michael Keen and Joel Slemrod.

Read More

Everyone is freaking out about potential increases in capital gains taxes. If I had a nickel for every time someone asked me if they should sell all their gains and take advantage of the low rate, I would have, by my accounting, about 85 cents (which is a lot—how often are you asked the same question 17 time!?!). For example, I recently got a call from a friend. She had bought a stock for $150,000 that was now worth $200,000. She knows President Biden wants to increase the capital gains tax, and hears that all the smart folks are selling their capital gains now to take advantage of the lower tax rate. She asked me what she should do. Sell now, to lock in that sweet lower capital gains tax rate, or sell later, and like a fool, pay a higher rate?

Read More