What Do We Know About the Effects of the Tax Cuts and Jobs Act?

On December 22, 2017, the U.S. tax code was dramatically changed when what is commonly referred to as the Tax Cuts and Jobs Act (TCJA) was signed into law. As tax scholars, we have a keen interest in knowing how the TCJA will change the world. On this page, we are posting empirical academic studies that focus on specific provisions of this monumental tax reform.

We plan to update this page as more studies come out. Further, many of these studies are early working papers, and have not been vetted by the peer-review process, so check back regularly for updates. While we will add new papers to this page, we will not update these papers as they go through the review process, are updated, published, etc. However, the information on this page should provide enough information for interested readers to track down the most up-to-date version of these papers.

Many of these articles below I have curated on my own, or others have shown to me. However, if you would like to request that we add your study, please email me at [email protected]. We are only posting studies that are hosted elsewhere (we prefer they be accessible on SSRN), and that are (1) empirical, (2) academic and (3) focus on the TCJA.

We study international spillovers of corporate tax reforms in a fragmented global tax regime. Using firm-level evidence on the 2017 U.S. Tax Cuts and Jobs Act (TCJA) and a quantitative general-equilibrium model, we illustrate how multinational enterprises (MNEs) propagate local policy shocks throughout the global economy. Our framework emphasizes two key intrinsic properties of intangible capital: non-rivalry and mobile ownership. We find the TCJA generated positive outward spillovers: First, it boosted U.S. MNEs’ intangible investment, raising their foreign subsidiaries’ output. Second, it increased tangible investment of foreign MNEs’ U.S. subsidiaries, incentivizing them to expand intangible investment at home. Conversely, a Global Minimum Tax (GMT) implemented by the rest of the world generates negative inward spillovers for the United States, even if U.S.-parented MNEs are exempt. These findings illustrate that there is no such thing as a purely domestic corporate tax policy.

Read More

Firms increasingly rely on external sources of innovation -- such as technology licensing, purchases of intangible assets, and business acquisitions -- to augment their internal R&D. We study whether external innovation complements or substitutes internal R&D using the 2022 enforcement of Section 174 of the Tax Cuts and Jobs Act as an exogenous shock that raised the after-tax cost of internal R&D. Using a difference-in-differences design, we show that more R&D-intensive firms significantly increased externally sourced innovation -- measured comprehensively using acquired intangible assets -- without reducing internal R&D. These firms subsequently achieved higher innovative efficiency and originality, explored new technological domains, were more likely to generate breakthrough patents, and became more profitable. The effects are significantly weaker among financially constrained firms and those in highly competitive industries, consistent with limited ability to reallocate resources toward external innovation. Analysis of inventor- and patent-level data supports a synergy channel, whereby collaborations between newly hired and incumbent inventors and greater technological proximity between external and internal innovations enhance innovation productivity. Overall, our findings provide causal evidence that external innovation complements, rather than crowds out, internal R&D, and that fiscal shocks to R&D incentives can reallocate capital and talent toward more productive innovation activities.

Read More

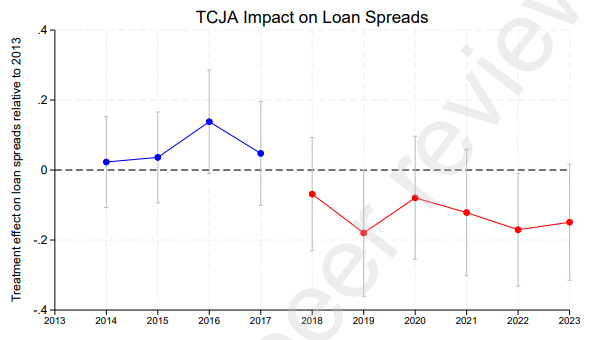

This paper examines how the 2017 U.S. Tax Cuts and Jobs Act (TCJA), a landmark corporate tax reform, affected the pricing and structure of syndicated bank loans. Using a difference-in-differences approach, we compare U.S. firms, which were directly exposed to the reform, with a matched sample of non-U.S. firms around the TCJA’s enactment. We find that U.S. borrowers experienced a significant reduction in loan spreads following the reform, consistent with lenders updating their expectations of improved firm cash flows and creditworthiness. The decline in loan spreads is more pronounced among firms with greater foreign exposure, higher tax savings, and tighter ex ante financial constraints. Additionally, we document adjustments in U.S. borrowers’ non-pricing loan terms, including a higher likelihood of covenant-lite provisions and a reduced incidence of collateral and performance pricing requirements. Overall, our findings highlight the importance of corporate tax policy in shaping financial contracting in private credit markets.

Read More

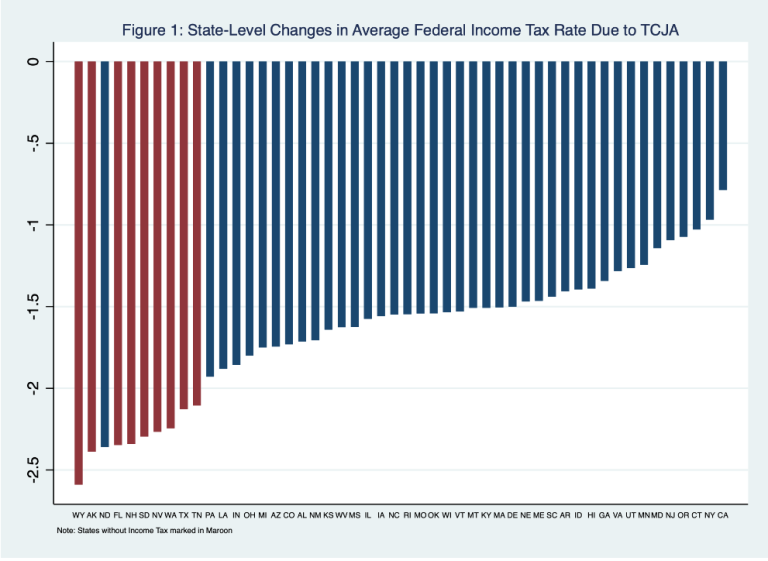

We develop a new method to estimate the effects of the 2017 Tax Cuts and Jobs Act (TCJA) on GDP that can be applied to both past and future reforms. Evaluating such reforms is difficult because provisions are broad and interrelated. To address this challenge, we combine abnormal stock returns during TCJA legislative windows with the pre-existing geographic distribution of firms to construct a county-level measure of exposure. Linking this measure to real outcomes, we estimate that the TCJA raised GDP by 1.8 percent, through higher investment, with gains concentrated in business income and older, wealthier counties.

Read More

This paper summarizes the significant changes to the taxation of business income in the United States over the last 25 years and how the resulting variation has helped inform research on business taxation. The survey of research on the topic covers investment incentives, international taxation, corporate financial policy, issues with pass-through businesses, compliance, enforcement, and other related topics.

Read More

The objective of this paper is to assess the influence of tax reductions from the Tax Cuts and Jobs Act ("TCJA"), on the firm value of non-publicly traded business organizations. The TCJA provided a reduction in the graduated corporate tax from a top rate of 35% to a flat 21%, while simultaneously providing up to a 20% deduction of taxable income produced by passthrough entities under Internal Revenue Code ("IRC") § 199A. While the overall value of non-publicly traded businesses increased after the TCJA, we find somewhat mixed results.

Read More

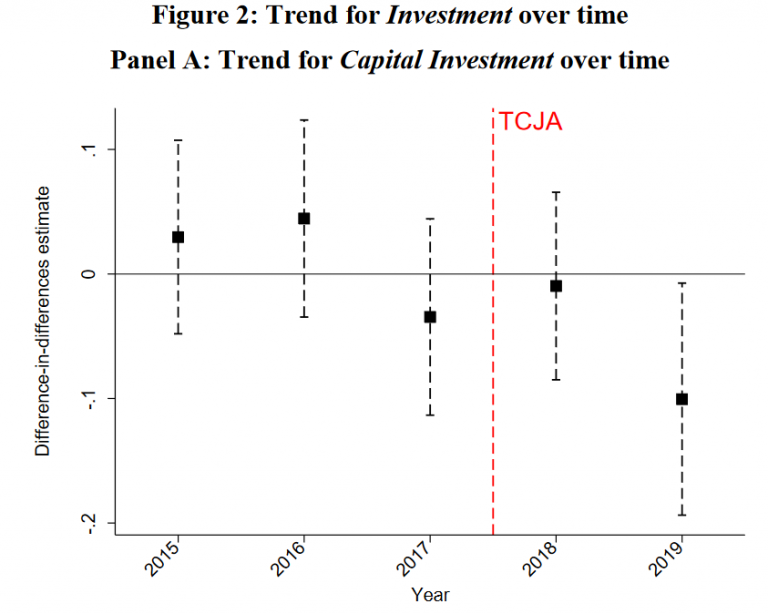

The 2017 Tax Cuts and Jobs Act (TCJA) represents the most significant tax overhaul since the Tax Reform Act of 1986, and one of the most substantial fiscal policies in American history. This paper examines the impact of the TCJA on capital investment in publicly traded U.S. manufacturing firms through 2020. It first outlines the corporate provisions of the TCJA, then delineates three classic theoretical models of how business investment should respond to tax cuts. The evidence indicates that the TCJA’s effect on investment was weaker than expected. Instead, firms redirected resources towards stock purchases and liquidity hoarding. These results, which strikingly diverge from theoretical expectations, highlight the need for further research linking tax policy and corporate behavior.

Read More

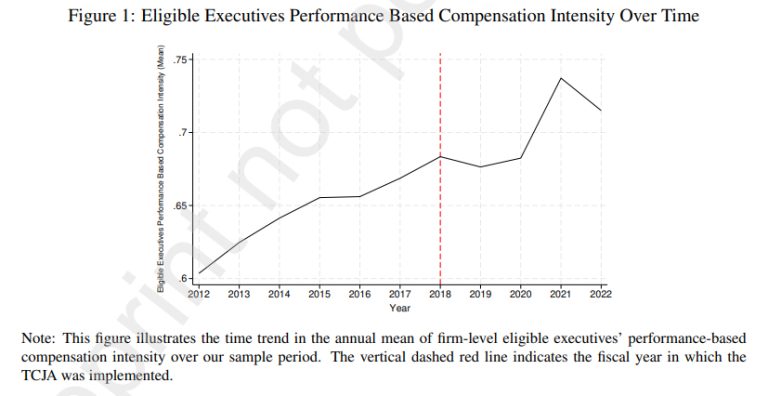

This paper examines how firms responded to a joint policy shock introduced by the 2017 U.S. Tax Cuts and Jobs Act (TCJA), which simultaneously replaced the progressive corporate tax schedule with a flat 21% rate and eliminated the deductibility of performance-based executive compensation under Section 162(m). We exploit cross-sectional variation in pre-reform reliance on performance-based pay and changes in marginal tax rates to show how ex-ante compensation structures shaped firm responses in innovation and intangible investment. We find that, relative to firms with lower pre-TCJA incentive-pay intensity, firms with higher exposure to ex-ante performance-based compensation increased R&D spending, patenting, and intangible investment after the reform—particularly when their marginal tax rates rose. These higher-exposure firms also reallocated performance-based pay away from tax-disfavored executives toward non-eligible executives. These effects are most pronounced in growth firms with high internal funding reliance. This pattern suggests a more complex relationship between executive pay design and intangible investment incentives under tax constraints.

Read More

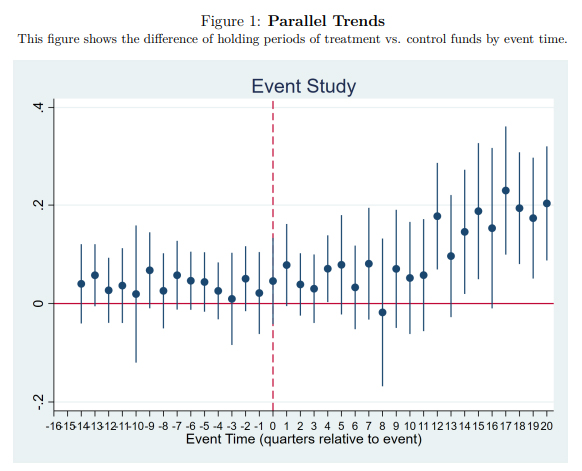

We document a novel dimension of agency issues among hedge funds. The 2017 Tax Cuts and Jobs Act (TCJA) extended the required holding period for carried interest to qualify for long-term capital gains treatment from one to three years. Using a difference-in-differences design, we find that funds subject to the rule significantly increased their investment horizons relative to unaffected funds. This effect is concentrated among funds with higher discretion and longer lockup periods. Our findings document an institutional lock-in effect, in which fund managers delay asset sales to preserve their own tax benefits at the expense of fund performance. We highlight an unintended distortion in capital allocation and investor outcomes from a tax law.

Read More

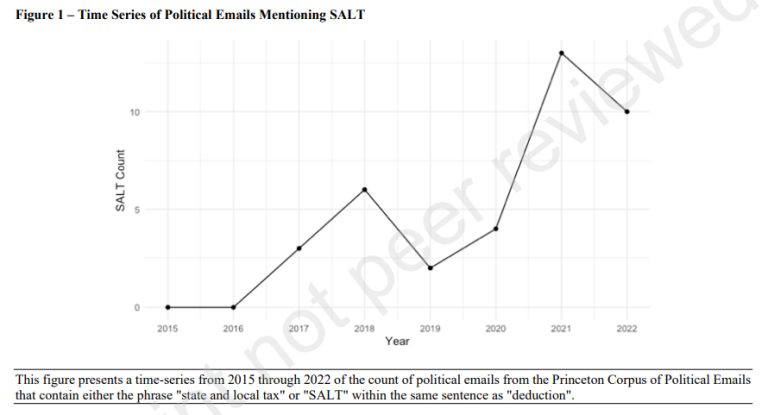

We investigate whether tax burdens affect political corruption. Higher tax burdens could increase government corruption by lowering after-tax income and incentivizing corruption. Alternatively, higher tax burdens may decrease corruption by increasing citizen political engagement and monitoring of politicians. We use the Tax Cuts and Jobs Act's (TCJA's) $10,000 cap on state and local tax (SALT) deductions and cross-county differences in property tax levels as plausibly exogenous variation in tax burdens. We find that future local political corruption convictions are associated with a 4.3% for every 1% increase in tax burdens. Further, we document that increased tax burdens raise voter turnout. We examine four different cross-sections of the data and find that the corruption reduction is more pronounced when expected. Together, our results provide evidence that tax burdens increase civic engagement and citizen monitoring of public officials, which in turn could contribute to lower corruption.

Read More

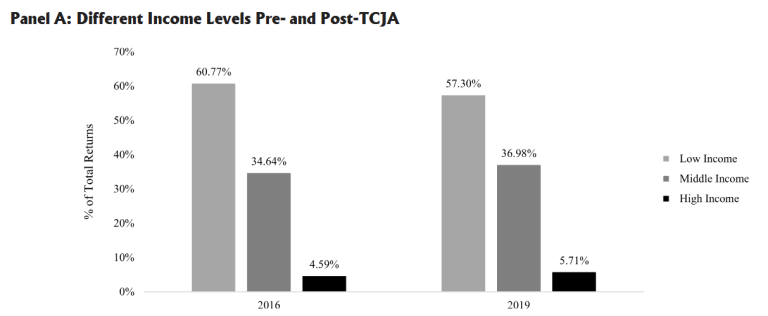

This is the first comprehensive, quantitative study of how the Tax Cuts and Jobs Act (TCJA) impacts individual taxpayers. Although this study has a specific focus on equity, it also broadly considers how the TCJA benefits and harms the tax system. Relative to equity, this study finds that the TCJA granted a roughly even tax cut across all income groups—on a percentage basis. However, as high-income taxpayers pay the majority of income taxes, this group received the largest tax cut in absolute dollars. Next, the results indicate that certain convenience-focused TCJA provisions (e.g., reduced itemized deductions) did not reduce related desirable economic activities (e.g., charitable giving), implying that these provisions were successful. Finally, the U.S. tax system raised similar tax revenues pre- and post-TCJA, implying that economic growth largely covered the costs of the Act. The study concludes by discussing how its findings inform policy and future studies.

Read More

We use publicly available information to estimate the country location of multinational firms’ cash holdings, examine why investors discount the value of cash held overseas, and examine whether that discount changes after the Tax Cuts and Jobs Act (TCJA) of 2017. We provide three main results. First, our firm-year foreign cash estimates are reasonably accurate, evidenced by high correlations with simulated data and proprietary country-level data, high adjusted R2 when explaining a firm’s total cash holdings, and the ability to replicate prior findings. Second, we demonstrate that investors value foreign cash holdings more negatively than domestic cash holdings when the cash is held in high agency-cost countries. Finally, we find that investors no longer appear to discount foreign cash after the TCJA, when the U.S. moved from a worldwide to a quasi-territorial taxation system.

Read More

The Tax Cuts and Jobs Act of 2017 (TCJA) marked the first time in three decades that material changes were made to the corporate tax code of the United States. We use TCJA as a quasi natural experiment to estimate the impact of changes in user cost of capital on investment. Following the method of Auerbach and Hassett (1991), using cross-sectional data we find that the user cost is associated with higher rates of investment consistent with previous studies. BEA asset types with greater reductions in user cost of capital and marginal effective tax rate (METR) after the 2017 TCJA had greater statistically significant increases in their investment rates several years after the tax reform. Specifically, we find the magnitude of a 1 percentage point decrease in user cost is associated with a 1.68 to 3.05 percentage point increase in the rate of investment, larger than prior estimates of the responsiveness of investment with respect to user cost of capital.

Read More

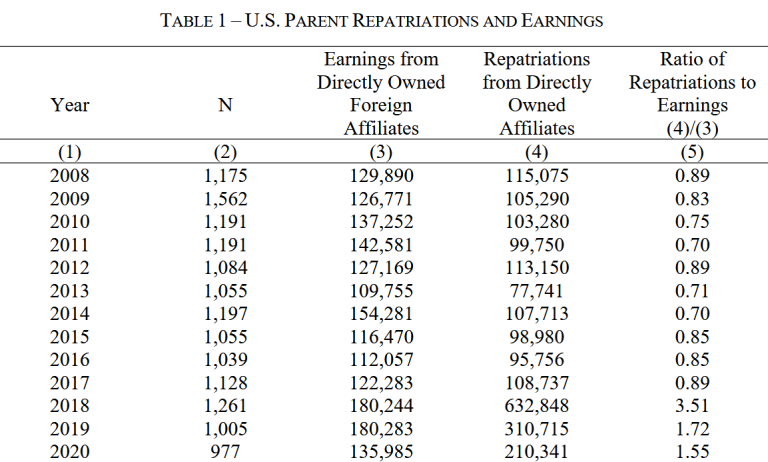

This study uses confidential information on foreign affiliate assets to investigate whether the Tax Cuts and Jobs Act of 2017 (TCJA) alleviated investment frictions created by permanently reinvested earnings (PRE) reported in U.S. multinational corporations' (MNCs) consolidated financial statements. We begin by investigating the repatriation behavior of MNCs surrounding enactment of the TCJA. Consistent with accounting creating frictions within the MNC, we document that repatriations are greater for firms with relatively more PRE held in cash. Relatedly, we find that domestic investment by MNCs with above median PRE held in cash is more sensitive to domestic cash flow than other firms before but not after the TCJA. Overall, our results are consistent with PRE being associated with internal capital market frictions which were alleviated after the TCJA.

Read More

The Tax Cuts and Jobs Act of 2017 (TCJA) introduced substantial changes to the U.S. corporate tax system, including a lower statutory tax rate and the adoption of a more territorial-like international tax framework. Many of the international provisions were meet with significant uncertainty regarding implementation and application for corporate tax positions. We present a theoretical framework that models a firm’s choice regarding the amount of risk firms are willing to take on their tax positions. We empirically test our predictions using measures of tax risk, uncertainty, and firm-level behavior before and after the TCJA. Our results suggest that the positive association between tax uncertainty and tax avoidance declines significantly after the TCJA, particularly for firms with tax haven subsidiaries. Our findings suggest that policy interventions that reduce incentives for elaborate tax planning can meaningfully reduce corporate tax risk-taking. This evidence provides insights for policymakers and stakeholders seeking to lower incentives for highly risky and aggressive tax planning strategies.

Read More

The Tax Cuts and Jobs Act of 2017 (TCJA) introduced substantial changes to the U.S. corporate tax system, including a lower statutory tax rate and the adoption of a more territoriallike international tax framework. These shifts carry important implications for the complexity of corporate tax positions. We present a theoretical framework that models a firm's choice regarding the complexity of tax positions. We then empirically test its predictions using measures of tax risk, uncertainty, and firm-level behavior before and after the TCJA. Our results suggest that the positive association between tax uncertainty and tax avoidance declines significantly after the TCJA, particularly for firms with tax haven subsidiaries. Contrary to recent claims that corporate tax complexity would persist or worsen without deliberate efforts to simplify the tax code, our findings suggest that policy interventions that reduce incentives for elaborate tax planning can meaningfully simplify corporate tax positions. This evidence provides insights for policymakers and stakeholders seeking to design more efficient and equitable tax systems.

Read More

The Tax Cuts and Jobs Act (TCJA) of 2017 represents the most significant reform of the U.S. income tax code since the Tax Reform Act of 1986. Previous analyses of the TCJA's economic impact often rely on projections based on data prior to the enactment of the legislation. This paper leverages plausibly exogenous variations in state-level tax changes brought about by the TCJA and employs local projections with two-way fixed effects to examine its effects on the labor market. Measures of TCJA tax shocks are constructed with the NBER-TAXSIM model using state-level tax return data from the Statistics of Income (SOI). Our findings suggest that tax cuts amounting to 1 percent of Adjusted Gross Income (AGI) under the TCJA are associated with a 1 percentage point increase in the labor force participation rate (LFPR) and a 1.5 percentage point acceleration in job growth over the two years following the TCJA's implementation. These results appear broadly robust to assumptions about heterogeneous state responses and the inclusion of interactive fixed effects.

Read More

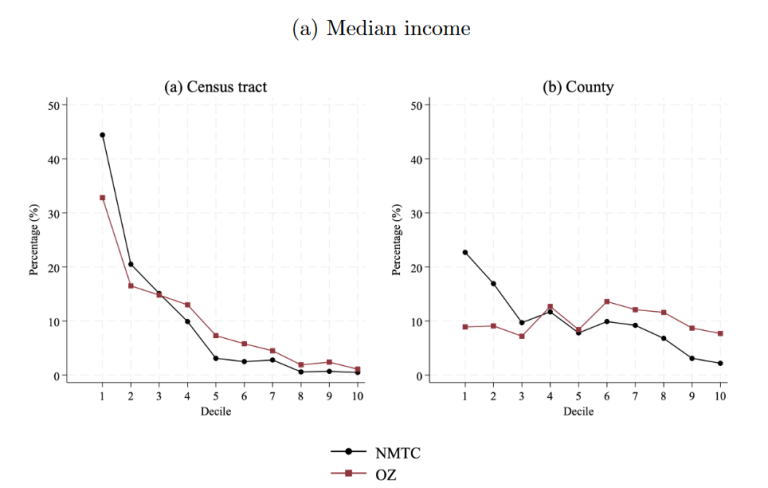

For a place-based policy to succeed, it must target the right areas—typically those with lower economic development and resident well-being. The U.S. has two major place-based tax policies: the New Markets Tax Credit (NMTC), where government- approved entities select investments, and Opportunity Zones (OZs), where private in- vestors choose projects. Despite underlying design differences, both target census tracts with high poverty rates, lower median income and weaker labor markets. However, OZs tend to attract more investment in areas with higher pre-existing private investment, often located in prosperous counties and high-growth regions. Census tracts lacking investment from either program generally show lower private investment, less home value growth, and less population growth, suggesting that additional policies may be needed to reach areas less primed for investment.

Read More

This paper documents that corporate tax planning innovations, proxied by decreases in effective tax rates, contribute to excess shareholder returns and, thereby, a competitive advantage. Compared to other improvements in firm performance, tax planning innovations have smaller factor loadings and explain fewer variations in excess returns. Notably, sales growth explains more than seven times the variations in excess returns compared to tax planning innovations. Tax planning even falls behind interest expense reductions, given the challenge of altering firm capital structure. To address the concern that changes in firm performance drive the association between tax planning innovations and excess returns, I explore the market reactions to the legislation events of the Tax Cuts and Jobs Act (TCJA). Consistent with a lower statutory rate reducing the benefit of tax planning, firms with stronger tax planning competitive advantage before TCJA experienced more negative market reactions. Overall, my study provides strong evidence of the competitive advantages of tax planning, albeit the magnitude is limited.

Read More

Venture capital (VC) funds are sophisticated asset managers that focus on generating returns for investors. Despite this fact, extensive research concludes that VC funds use a tax-inefficient organizational form for their investments (i.e., startups), incurring a tax cost of about 5% of funds’ invested capital. Using a model that more fully incorporates VC fund taxation, we find the opposite result: analyzing the same data as prior research, we find that VC funds save about 8% of invested capital by using their startups’ current organizational form versus the alternative. However, this advantage is not borne equally by investors, including fund managers who face additional tax costs under the current organizational form. We also find that the Tax Cuts and Jobs Act of 2017 reduces the tax advantage of VC-backed startups’ current organizational form. Our model informs VC fund managers evaluating organizational form choice and policymakers considering potential outcomes of tax changes.

Read More

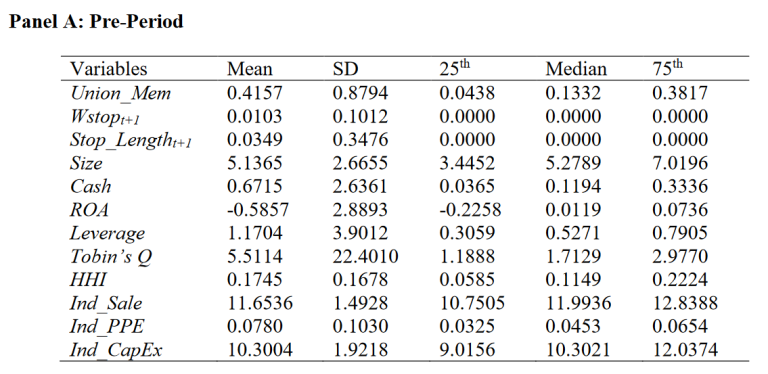

This study examines the impact of the Tax Cuts and Jobs Act of 2017 (TCJA) on domestic labor union bargaining strength faced by U.S. multinational corporations (MNCs). Before TCJA, U.S. MNCs operated under a worldwide tax system that imposed incremental U.S. taxes on earnings repatriated from overseas, prompting MNCs to leave large cash balances abroad while simultaneously allowing them to strategically shelter cash from domestic union demands to preserve their bargaining power. The TCJA resolves such “trapped cash” concerns by allowing U.S. MNCs to repatriate foreign cash without incurring incremental U.S. tax. This allows domestic workers to access previously sheltered foreign cash reserves, thereby strengthening the bargaining power of unions representing domestic workers. Consistent with our prediction, we find that MNCs become more vulnerable to both potential and enacted collective bargaining power of labor unions after TCJA, evidenced by increases in union membership rates and both the frequency and duration of strikes, respectively. In additional analyses using an entropy-balanced sample of MNCs, we provide supporting evidence that TCJA’s “unchaining” of previously trapped foreign cash is the primary channel through which potential union strength increases ex-post.

Read More

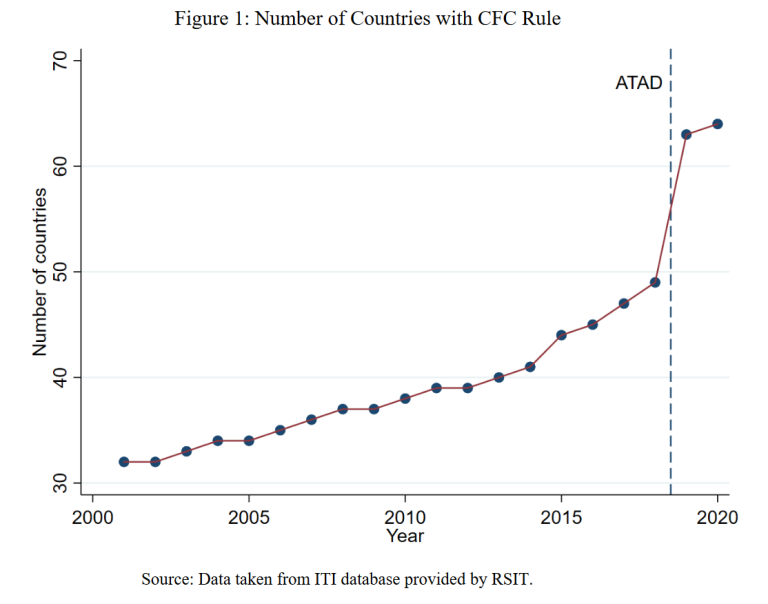

This chapter provides a description of one of the key anti-tax-avoidance rules to combat profit shifting by multinational corporations, so called Controlled Foreign Corporation (CFC) rules that directly target income in low-tax countries. We explain some key institutional features of CFC provisions. We then present some data and descriptive statistics before we review existing theoretical and empirical research analyzing CFC rules. Our review also includes the new U.S. GILTI rules. CFC rules are effective in curbing profit shifting, but their effect on the real economy is still unclear. In contrast, GILTI seems to be ineffective when it comes to profit shifting, but it has consequences for real activity. We finally argue that research on CFC regulations and GILTI can be informative in assessing the recent global minimum tax initiative.

Read More

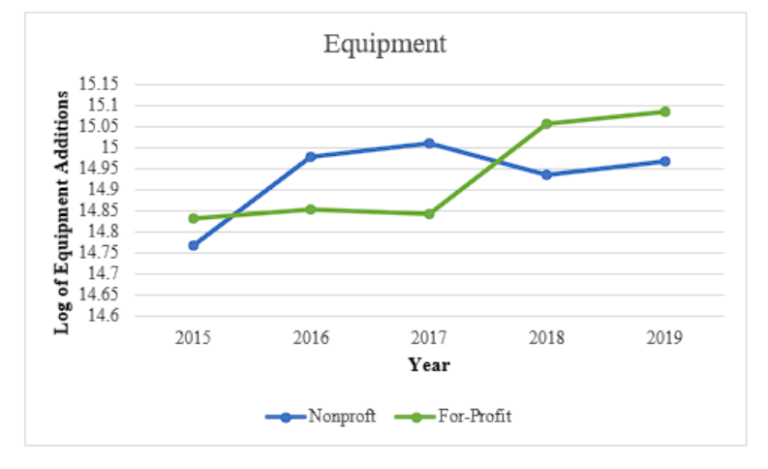

We examine how the Tax Cuts and Jobs Act of 2017 (TCJA) altered the hospital industry. Nonprofit hospitals make up approximately 80 percent of all hospitals and generally have an advantage over their for-profit counterparts due to their tax-exempt status. Provisions in the TCJA exogenously increase the relative cash flow in for-profit hospitals compared to nonprofit hospitals. We hypothesize and find that this comparative change in tax-driven cash flows results in greater investment, primarily in capital assets, among for-profit hospitals relative to nonprofit hospitals. We then test for changes in the quality of care around the TCJA and present evidence of a reduction in relative readmissions among for-profit hospitals, indicating an increase in for-profit quality of care. Lastly, using financial data from California hospitals, we find that the TCJA reduced implicit taxes among for-profit hospitals. Our results contribute to the tax literature by providing initial evidence of how a shift in tax policy altered the dynamics of the hospital industry.

Read More

The Tax Cuts and Jobs Act (TCJA) is one of the most significant US tax reforms in 40 years. However, we know little about the TCJA’s macroeconomic effects, presumably due to the difficulty in distinguishing the law’s effects from other factors that affect the macroeconomy. In this paper, I create a new methodology that allows a researcher to use firms’ market reactions to identify the effects of a macroeconomic shock on the broader economy. I apply this method to the TCJA to identify its effects on GDP and wages. I find that the TCJA increased GDP and total wages paid to employees by 2.2% and 3.4%, respectively. I find that the total wage increase was driven by a 1.7% increase in employment and a 1.3% increase in annual salaries. In other words, I find the TCJA created 2 million jobs and increased average annual salaries by $520.

Read More

This paper combines administrative tax data and a model of global investment behavior to evaluate the investment and firm valuation effects of the Tax Cuts and Jobs Act (TCJA) of 2017, the largest corporate tax reduction in the history of the United States. We extend the canonical model of Hall and Jorgenson (1967) to a multinational setting in which a firm produces in domestic and international locations. We use the model to characterize and measure four determinants of domestic investment: domestic and foreign marginal tax rates and cost-of-capital subsidies. We estimate elasticities of domestic investment with respect to each and use them to identify the structural parameters of our model, to quantify which parts of the reform mattered most to investment, and to conduct policy counterfactuals. We have five main findings. First, the TCJA caused domestic investment of firms with the mean tax change to increase by roughly 20% relative to firms experiencing no tax change. Second, the TCJA created large incentives for some U.S. multinationals to increase foreign capital, which rose substantially following the law change. Third, domestic investment also increases in response to foreign incentives, indicating complementarity between domestic and foreign capital in production. Fourth, the general equilibrium long-run effects of the TCJA on the domestic and total capital of U.S. firms are around 6% and 9%, respectively. Finally, in our model, the dynamic labor and corporate tax revenue feedback in the first 10 years is less than 2% of baseline corporate revenue, as investment growth causes both higher labor tax revenues from wage growth and offsetting corporate revenue declines from more depreciation deductions. Consequently, the fall in total corporate tax revenue from the tax cut is close to the static effect.

Read More

This paper studies the impacts of limiting interest deductions on firms’ investment and financing choices using U.S. tax data. The 2017 law known as the Tax Cuts and Jobs Act (TCJA) implemented an interest limitation for big, high-interest firms. Using an event study design comparing big and small high-interest firms, we rule out economically significant impacts of the interest limitation on investment and leverage, and find evidence that the interest limitation led firms to increase their equity issuance. A triple difference design that accommodates size-varying impacts of other TCJA policy changes yields similar results, as does a regression discontinuity design focusing on marginal firms that are just large enough to face the interest limitation. Our results indicate many firms do not use debt as their marginal source of financing and provide evidence consistent with capital structure models with fixed leverage adjustment costs. Furthermore, our results suggest limiting interest deductions is unlikely to have large impacts on investment or to address concerns about rising corporate debt levels.

Read More

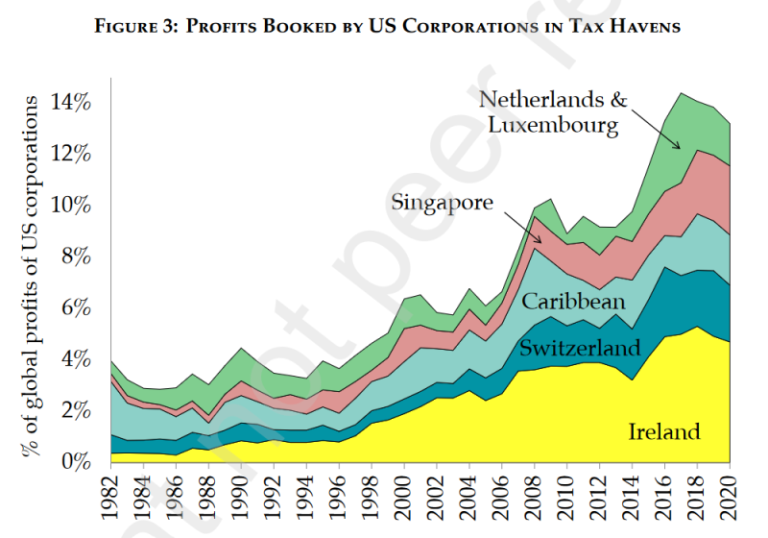

The 2017 Tax Cut and Jobs Act reduced the US corporate tax rate and introduced provisions to curb profit shifting. We combine survey data, tax data, and firm financial statements to study the evolution of the geographical allocation of US firms’ profits after the reform. The share of profits booked abroad by US multinationals fell 3–5 percentage points, driven by repatriations of intellectual property to the US. The share of foreign profits booked in tax havens remained stable around 50% between 2015 and 2020. Changes in the global allocation of profits are small overall, but some firms responded strongly.

Read More

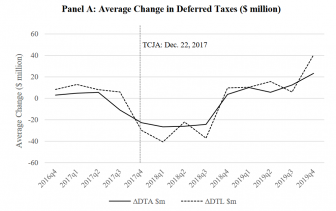

We take advantage of a 2017 change in tax rules in the U.S. to re-examine whether CEOs are rewarded for luck. We examine the effect of one-off tax gains and losses associated with deferred tax assets and liabilities on CEO compensation around the Tax Cuts and Jobs Act (TCJA) of 2017. Relative to other years, we find that less visible firms compensated their CEOs more for the one-time tax windfall gains during the TCJA-transition period. Further, we find evidence in support of pay asymmetry; CEOs of less visible firms were compensated more for tax windfall gains but were not compensated less for tax windfall losses. The CEO pay associated with the tax windfalls cannot be explained as firms sharing these tax gains with all employees. These results are consistent with rent-extraction by CEOs of less visible firms.

Read More

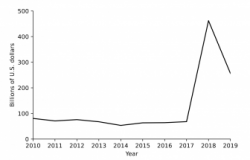

The Tax Cuts and Jobs Act removed the repatriation tax on the accumulated foreign profits of U.S. firms, effective January 1, 2018. Overnight, this unlocked as much as $1.7 trillion in new liquidity for U.S. multinationals. Using a difference-in-differences approach, we examine the real and financial response to this liquidity shock. We find that firms did not increase capital expenditures, employment, R&D, or M&A in response to the increased access to cheap capital, regardless of financial constraints. On the financial side, firms responded to the increased liquidity by increasing share repurchases and adjusting downward consolidated cash holdings. However, less than one-third of this new liquidity was paid out to shareholders, and half of it was retained as cash. This high retention was not associated with poor governance. Our findings suggest a low sensitivity of financial positions in response to liquidity shocks even among well-governed firms with limited financial constraints.

Read More

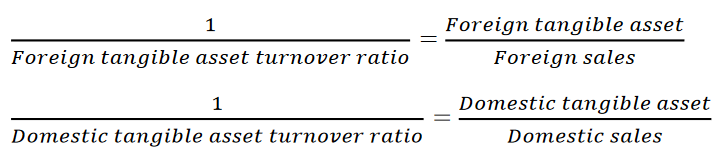

The U.S. tax reform in 2017 introduced the Global Intangible Low-Taxed Income (GILTI) tax to discourage U.S. multinational companies (MNCs) from shifting intangible income offshore. The reform simultaneously introduced the Foreign Derived Intangible Income (FDII) tax incentive to encourage companies to locate intangible income derived from export sales in the United States. We examine whether and how these two tax provisions affect the investment decisions of U.S. R&D-intensive MNCs. We find that these MNCs increase foreign tangible investments to minimize their GILTI tax burden but do not appear to decrease domestic tangible investments. To maximize FDII tax benefits, MNCs increase investments in both foreign and domestic human capital. We find MNCs are more likely to increase foreign human capital when they have more cross-border collaboration experience, consistent with the prediction that firms increase foreign R&D to better adapt home-developed technology for foreign markets. We further show that FDII incentivizes MNCs to cultivate a new R&D workforce in the U.S., as opposed to merely recruiting seasoned R&D personnel from other firms. Our findings have timely implications for policymakers to assess the impact of the 2017 tax reform.

Read More

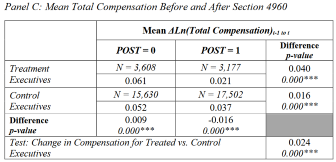

We examine the effect of Internal Revenue Service code (IRC) section 4960 of the Tax Cuts and Jobs Act of 2017 (TCJA) which imposed a 21% excise tax on nonprofit employee compensation over $1 million per covered individual. Using a difference-in-differences analysis on IRS Form 990 data for almost 40 thousand nonprofit employee-year observations from 2015 to 2020, we find a lower growth rate for treated employee compensation post section 4960. Our results are robust to the use of alternative treatment specifications as well as control samples, e.g., employees earning more than $1 million but not covered under section 4960; medical professionals specifically exempt from section 4960. We also find that CEO turnover is higher for treated CEOs post section 4960. Our findings contrast those of prior research on Section 162, the parallel provision which applies to executive compensation in for-profit publicly listed firms, which found no decrease in compensation.

Read More

We examine the firm value effects of Treasury Regulations, a powerful source of tax law that prior research has largely overlooked. The hasty enactment of the Tax Cuts and Jobs Act (TCJA) left interpretive gaps for Treasury to fill. We employ Treasury Regulations related to the TCJA’s global intangible low-taxed income (GILTI) provisions as an identifiable setting that impacts many firms. We predict that investors will react negatively (positively) to regulations that investors expect to increase (decrease) firms’ future tax burdens or the uncertainty thereof. We identify firms affected by GILTI through their disclosures and find significant market reactions for these firms around the issuance of Treasury Regulations related to the GILTI provisions. Importantly, we find that these reactions vary cross-sectionally on observable characteristics and that institutional investors drive these reactions. The study improves our understanding of how administrative law shapes tax policy by documenting shareholder reactions to Treasury Regulations.

Read More

We exploit the 2017 US tax reform to learn about the tax-competitiveness of US multinational corporations (MNCs) relative to their international peers. Matching on the propensity score, we compare pairs of similar US and European firms listed on the S&P500 or StoxxEurope600 in a difference-in-differences setting. Our results suggest significantly lower effective tax rates of US MNCs compared to their European competitors after the US tax reform. Additional tests show (i) that US MNCs have gained substantially in what we call tax-competitiveness, (ii) that the reform effect is more pronounced for MNCs with a high share of domestic activity, and (iii) that the tax reform did not change the international tax-planning behavior of US MNCs. We provide evidence that US MNCs already successfully engaged in international tax planning prior to the reform, and this behavior is unchanged after the tax reform.

Read More

This study examines the effect of the 2017 Tax Cuts and Jobs Act (TCJA) on capital investment, labor investment, and the productivity of foreign subsidiaries of U.S. multinational corporations (MNCs). Proponents of the TCJA argue it decreased foreign investment by leveling the playing field between U.S. MNCs and foreign-owned corporations. However, policymakers are currently debating international tax reform, arguing that the TCJA incentivizes foreign investment. My study informs this debate by providing empirical evidence on the TCJA’s effect on foreign investment and productivity. Using a difference-in-differences design, I find that after the TCJA, U.S.-owned foreign subsidiaries invest 13.1 percent less in capital and 1.3 percent less in labor relative to subsidiaries owned by non-U.S. MNCs. I also find these reductions are positively associated with subsidiary-level productivity, suggesting that the TCJA alleviates inefficiencies of the previous tax regime.

Read MoreThis study examines the impact of the Tax Cuts and Jobs Act of 2017 (TCJA) on U.S. corporate investment. We examine U.S. firms and compare them to Canadian firms from 2017 to 2019 in a multivariate firm fixed-effects difference-in-differences analysis. Our results indicate that investment increases for U.S. firms relative to Canadian firms after the tax cuts. We also find that firms with high levels of cash held abroad before the tax cuts and those that shift the most cash back to the U.S. after the tax cuts increase investment the most. Furthermore, we exploit a provision in the TCJA that allows firms to immediately deduct the full cost of assets with lives of less than 20 years by showing that the increase in investment is concentrated among firms with shorter asset lives. Finally, we show that for U.S. based firms, assets increase for their domestic but not their foreign operations. The paper contributes to the literature by providing systematic evidence on the effects of the TCJA which have been debated extensively by politicians, journalists, tax policy experts, and academics.

Read MoreThis paper analyzes stock market reactions to announcements of cross-border M&A deals before and after the ‘Tax Cuts and Jobs Act of 2017’ (TCJA). Prior literature established that the repatriation tax system resulted in agency conflicts and correspondingly low announcement returns due to excess cross-border acquisitions. The TCJA abolished the repatriation tax. Therefore, M&A decisions by the managers might more closely align with the investors’ perspective post TCJA. Correspondingly, announcement returns could become more positive. However, if managers continue to pursue excess cross-border acquisitions, investors might be particularly dissatisfied because of the alternative option of tax-exempt repatriation post TCJA. In line with excess M&A acquisitions post TCJA, I present evidence that abnormal returns to cross-border M&A announcements by U.S. firms are significantly lower in the period after the TCJA. The effects are concentrated in U.S. acquirers most affected by the repatriation tax prior to the TCJA, in cross-industry deals, and in acquisitions by firms with low leverage and low payout ratios. Overall, my findings suggest that the negative perception of cross-border M&A is driven by agency conflicts not solved by the TCJA.

Read MoreThe target’s valuation is the cornerstone of merger negotiations and hinges on expectations of after-tax cash flows. But how do buyer and seller adapt when the underlying tax parameters are in flux? Focusing on the months-long legislation process behind major corporate tax reform in 2017 (TCJA) and exploiting hand-collected data on private merger negotiations, we examine in real time the impact of tax reform and its uncertainty on contemporaneous merger negotiations. Acquisition premiums negotiated during tax legislation are increasing in the target’s expected gain from tax reform. Tax legislation events are rapidly followed by new private merger negotiations, especially when the target’s expected tax reform gains are high. For deals negotiated during tax legislation, the magnitude of pre-announcement bid revisions are increasing in the target’s expected gains from the reform and driven by targets with more bargaining power. Our results provide new insight on takeover negotiation responses to material but uncertain tax policy events.

Read MoreThis paper studies the impact of a place-based tax credit policy, the Opportunity Zone program created under the Tax Cuts and Jobs Act of 2017, on local private investments and entrepreneurship. Using a difference-in-differences approach and comparing census tracts designated as Opportunity Zones and other eligible but non-designated tracts, I find that the policy has drawn significantly more private investments to economically distressed areas. Surprisingly, however, these private investments have led to decreases in local new business registration. The decrease in entrepreneurship was mainly in the non-tradable sector, which is more sensitive to local conditions than the tradable or construction sector. Further robustness tests suggest that the above results are causal. I provide one explanation for the above findings that more private investments went to existing and older firms in Opportunity Zones, discouraging potential entrepreneurs from competing with the better-financed firms locally.

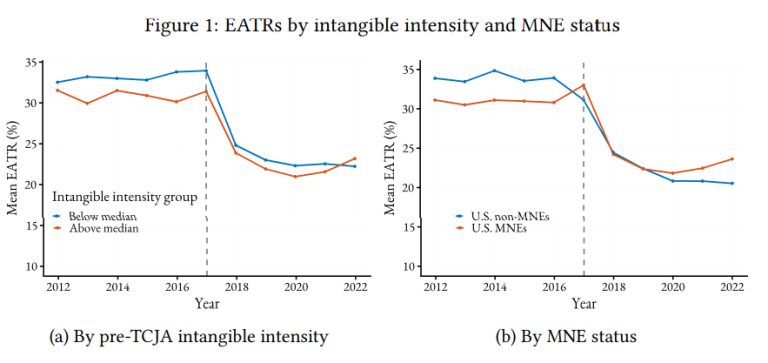

Read MoreThe 2017 Tax Cuts and Jobs Act (TCJA) sharply reduced effective corporate income tax rates on equity-financed US investment. This paper examines the reform’s impact on US inbound foreign direct investment (FDI) and investment in property, plant and equipment (PPE) by foreign-owned US companies. We first model effective marginal and average tax rates (EMTRs and EATRs) by country, industry, and method of finance, and then use those tax rates to calculate the tax semi-elasticities of inbound FDI and PPE investment. We find that both PPE investment and FDI financed with retained earnings responded positively to the TCJA reform, but FDI financed with new equity or debt did not. In country-level PPE regressions, inclusion of macroeconomic controls renders tax rate coefficients insignificant, suggesting that the increase in PPE investment after TCJA was driven by general economic growth. In regressions of FDI financed with retained earnings, however, tax coefficients were robust to inclusion of macroeconomic controls. As the literature predicts, EATRs have a greater impact on cross-border investment than EMTRs. Country-by-industry regressions showed a larger effect of taxes on PPE investment than aggregate country-level regressions, but industry-level tax rates appear to have no effect on earnings retention.

Read MoreA provision of the Tax Cuts and Jobs Act of 2017 offered tax incentives for investing in certain low-income areas in the United States called Opportunity Zones (OZs). The goal of this provision was to spur private investment in OZs in order to improve the economic well-being of their residents. This paper uses a regression discontinuity design to evaluate the impact of OZs on commercial investment and economic activity. Using data on the universe of all significant commercial investments in the United States, we find that OZ selection led to practically no increase in investment in OZs. These findings are supported by additional data from Mastercard that also show no evidence of increased business activity nor consumer spending. Overall, our findings suggest that the impact of OZs on economic improvement has thus far been limited.

Read MoreThis paper extends a standard general equilibrium framework with a corporate tax code featuring two key elements: tax depreciation policy and the distinction between c-corporations and pass-through businesses. In the model, the stimulative effect of a tax rate cut on c-corporations is smaller when tax depreciation policy is accelerated, and is further diluted in the aggregate by the presence of pass-through entities. Because of a highly accelerated tax depreciation policy and a large share of pass-through activity in 2017, the theory predicts small stimulus, large payouts to shareholders, and a dramatic loss of corporate tax revenues following the Tax Cuts and Jobs Act (TCJA-17). At the same time, because of less accelerated tax depreciation and a lower pass-through share in the early 1960s, the theory predicts sizable stimulus in response to the Kennedy’s corporate tax cuts. The model-implied corporate tax multiplier for Kennedy’s tax cuts is four times higher than for the TCJA-17. These predictions are consistent with novel micro- and macro-level evidence from professional forecasters and publicly available tax returns. The paper also offers analytic insights that clarify how these results relate to the capital taxation literature in macroeconomics.

Read MoreHow do global minimum taxes affect corporate balance sheets and real activities? I study this question using the introduction of the base erosion and anti-abuse tax (BEAT) on multinational insurance companies operating in the US. I find that the BEAT implementation significantly changed the internal capital allocation of insurers, increased global risk-sharing, and increased product prices in the US. I document three main sets of findings. First, the global minimum tax significantly changed the internal capital allocation of insurance companies and decreased the amount of transfer payments of US insurers to their foreign affiliates by 59%, or $30 billion per year. The changes in allocation were primarily driven by foreign-domiciled insurance groups and insurance groups which used foreign affiliates more extensively prior to the tax reform. Second, the tax increased global risk-sharing, inducing insurers to diversify more risk with external counterparties. Revealed-preference estimates suggest that the total increase in risk-sharing is worth $1.9 billion per year for insurers, equal to 2.9% of insurers’ total net income. Third, insurance companies affected by the minimum tax increased policy prices by 1.03% relative to not-affected insurers.

Read MoreThe US Tax Cuts and Jobs Act (TCJA) led to a drastic reduction in the corporate tax and improved the treatment of C corporations compared to S corporations. We study the differential effect of the TCJA on these types of corporations using key economic variables of US banks, such as the number of employees, average salaries and benefits, profit/loss before taxes, and net income. Our analysis suggests that the TCJA increased the net-of-tax profits of C corporation banks compared to S corporations and, to a lesser extent, their pre-tax profits. At the same time, the reform triggered no significantly differential effect on the employment and average wages.

Read MoreThis paper examines the effects of the 2017 U.S. tax reform, commonly known as the ‘Tax Cuts and Jobs Act’ [TCJA] on cross-border M&As of U.S. acquirers. The TCJA replaced the U.S. worldwide tax system by a territorial system, albeit with one important exception: the ‘Global Intangible Low-Taxed Income’ [GILTI] provision. Our results suggest that the outbound acquisition pattern changed significantly for those U.S. acquirers that are affected by the new GILTI provision. GILTI-affected firms acquire targets in low-tax countries and tax havens significantly less often after the TCJA. We also provide weak evidence that U.S. firms not affected by the GILTI regime acquire more often targets in low-tax countries and tax havens.

Read More

We find U.S. multinational corporations (MNCs) responded to the Tax Cuts and Jobs Act (TCJA) of 2017 by increasing income shifted to foreign sources in the first two years following the effective date. Financially constrained MNCs increased income shifting more, while higher operational uncertainty MNCs increased income shifting less than other MNCs. Moreover, MNCs likely to be subject to the base erosion and anti-abuse tax (BEAT) increased income shifting less than other MNCs, while firms having a global intangible low-taxed income (GILTI) inclusion are not discouraged from shifting income. MNCs that increase income shifting the most disclose less information about their GILTI liabilities. Our findings suggest that the GILTI provisions are not effective in curbing income shifting to foreign jurisdictions and that proposals such as the Global Minimum Tax are also unlikely to be effective if the rate is lower than the home country corporate income tax rate.

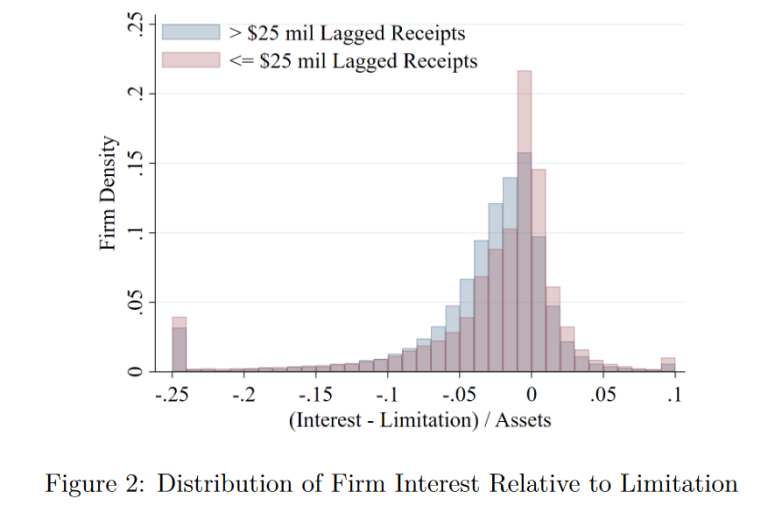

Read MoreDespite extensive efforts, the relation between tax incentives and corporate capital structure is an open question. The 2017 US tax reform creates an opportunity to directly estimate this relation. The reform limits the tax advantage of debt for all firms except for small businesses with average sales below $25 million. I use the exception threshold in a regression discontinuity design and show that corporate debt declines nearly dollar for dollar as the present value of the tax benefits of debt shrinks. Treated firms do not raise equity to replace debt, and they decrease investments and hiring, consistent with a rise in the cost of external financing. Confirming the tax channel, treatment effects are stronger in firms with more profits and smaller non-debt tax shields. Comparing the size of the debt tax shield across the firm size distribution suggests that the estimates likely provide a lower bound for the effects in large corporations.

Read MoreWe use electronically-filed federal tax records from tax year 2019 to document the first available evidence on the short-run response of financial capital to the Opportunity Zone (OZ) program, a federal place-based policy that provides tax incentives for capital investments in more than 8,000 low-income neighborhoods across the United States. We observe $18.9 billion of aggregate OZ investments from electronic filers in tax year 2019. While these data do not yet incorporate paper filers, several suggestive patterns emerge. First, OZ capital appears highly spatially concentrated: 84% of designated Opportunity Zone tracts in our sample receive zero OZ investment, and among those that do receive investment, the distribution is highly skewed. Second, we correlate OZ capital with tract-level demographic characteristics and show that, although tracts that receive investment are disadvantaged relative to the general US population, they appear well-off relative to other OZ tracts that do not receive investment. Among OZ tracts, investors report equity and property investments in neighborhoods with relatively higher incomes, home values, educational attainment, and pre-existing income and population growth. These tracts have also experienced significant changes in their demographic composition over the past decade. Finally, we geocode the universe of individual and business tax records to construct novel tract-level measures of wages, employment, commuting, firm growth, and real investment that we plan to use to evaluate the causal effect of the OZ tax subsidies as more comprehensive data become available. We demonstrate that these estimates closely match corresponding measures from publicly available Census data. We explicitly discuss limitations of the data, and will update this working paper as more comprehensive data become available.

Read MoreThe Tax Cuts and Jobs Act of 2017 (TCJA) reduces U.S. multinational companies’ (MNC) internal capital market frictions related to repatriation costs by decreasing costs to access internal capital (i.e., foreign cash). This study examines MNCs’ responses to the TCJA and finds spending and investment behavior are dependent upon liquidity, investment opportunities, and borrowing costs. Domestic capital expenditures increased for MNCs with low domestic liquidity and high domestic investment opportunities. These firms also increased share repurchases. In contrast, MNCs with low domestic liquidity and low domestic investment opportunities increased dividends. MNCs with low domestic investment opportunities and high cost of debt reduced their outstanding debt. We also investigate responses to global intangible low-taxed income (GILTI) incentives and find that MNCs with more foreign cash and a greater likelihood of being affected by the GILTI regime increase their foreign but not domestic capital expenditures - a potential unintended consequence of TCJA.

Read MoreWe consider the short-run responses of businesses and their owners to the introduction of Section 199A, a deduction implemented in 2018 that reduced the effective tax rate on pass-through business income. We study the deduction using several datasets derived from de-identified tax records of individuals and businesses. Overall, we do not find an increase in 2018 in business income likely to be eligible for the deduction, either in the time series or among firms with greater exposure to the deduction due to plausibly exogenous characteristics. We additionally examine specific hypothesized margins of adjustment. We find that partnerships (one type of pass-through business) reduce compensation paid to owners, in line with the incentives created by 199A, but that S corporations (another type of pass-through business) mostly do not. Additionally, we do not find that workers – whether new hires or current employees – switch from employee to contractor status to claim the new deduction. Finally, we find no evidence of changes in real economic activity as measured by physical investment, wages to non-owners, or employment of nonowners, though this analysis is underpowered in the short-run.

Read MoreAuthors estimate the market anticipated the probability of TCJA passage to be as high as 95% 30 days before the event. The full value impact of the TCJA is found to be 12.36%, compared to 0.68% when market anticipation is ignored.

Read MoreCorporate defined-benefit (DB) pension sponsors in the US are increasingly on a path of “derisking” – by moving pension assets away from equities and towards fixed-income securities that better match the obligations, or by transferring obligations off their balance sheets entirely, via settlements with insurance companies or lump-sum payouts to beneficiaries. In this study, we examine whether the Tax Cut and Jobs Act of 2017 (“TCJA”) served as a driver of pension derisking. Examining behavior in the window between the TCJA’s announcement and its lower tax rate going into effect, we document that sponsors with stronger incentives to derisk their pensions tend to contribute more into their plans in that window, while deductions can still be taken at the higher tax rate – specifically, sponsors expecting large and uncertain contribution requirements for pensions in the future, facing high regulatory costs to maintaining plans, and with competing demands on cash flows. Examining behavior after the TCJA goes into effect, we document that the firms with the largest TCJA-triggered contributions also engage in more derisking subsequently, both by shifting asset allocations and by transferring obligations to other parties. In sum, our findings point to the TCJA having acted as a trigger for what could be a fundamental reorganization of the DB pension landscape in the US.

Read MoreApproximately 60 public companies announced they would share cash windfalls from the Tax Cuts and Jobs Act (TCJA) with rank-and-file employees through bonuses, higher wages, or increased benefits. We use employee survey data from Culture X to examine how the announcement of these TCJA bonuses affected employee pay satisfaction. Although employees are economically better off upon receiving these bonuses, prior literature suggests employee pay satisfaction could decrease if employees perceive the bonuses to be unfairly small. Using a difference-in-difference design, we find a greater decline in pay satisfaction among employees at firms announcing a TCJA bonus versus those that do not. Consistent with dissatisfaction about unfairly small bonuses, we document a larger decline in pay satisfaction at announcing firms with larger increases in CEO bonuses and larger share repurchases around the TCJA. Our results provide new insights into how workers respond to changes in compensation stemming from corporate tax savings.

Read MoreThis study examines whether multinational corporations (MNCs) reclassify related-party payments to avoid the new base erosion and anti-abuse tax (BEAT). The Tax Cuts & Jobs Act of 2017 included the BEAT to combat income shifting from the U.S. to foreign entities. An exclusion in the tax law provides MNCs an incentive to reclassify related-party payments as cost of goods sold. We use a triple-difference design that leverages the BEAT filing threshold of $500 million in revenue and the parent company’s location to document increases in the unconsolidated sales of foreign subsidiaries of MNCs subject to BEAT relative foreign subsidiaries of MNCs not subject to BEAT consistent with cost reclassification. We also find this effect is strongest in MNCs with more related-party payments. Overall, our results imply that firms use the subjectivity inherent in cost classification to reclassify costs as cost of goods sold to avoid the BEAT.

Read MoreWe examine the impact of changes in the federal tax treatment of owner-occupied housing stemming from the implementation of the Tax Cuts and Jobs Act (TCJA) in January 2018 on local housing markets. Using county-level house price information and IRS tax data, we find that, holding everything else the same, capping the federal tax deduction of state and local taxes at $10,000 has caused the growth rate of home value to decline by an annualized 0.9 percentage point, or 18 percent, in areas where real estate taxes as shares of taxable income exceeded the national median. The results are robust when controlling for other changes in the tax reform. The areas with a high real estate tax burden also suffered from reductions in market liquidity after the reform. Fewer houses were transacted either in absolute numbers or as shares of total listings and houses stayed on the market longer before being sold. Importantly, we find that the housing market slowdown was accompanied by declines in local construction employment growth as well as multi-family building permits. Furthermore, on net more people moved out of these areas after the reform. Finally, we show that the act has already had political consequences. In the 2018 midterm Senate elections, more voters voted for Democratic candidates in areas with high real estate tax burden than they did for Republican candidates.

Read MoreAs part of the most sweeping federal tax reform in a generation, the Tax Cuts and Jobs Act (“TCJA”) radically altered the tax treatment of compensation paid to senior executives of public companies. Prior to the TCJA, payment of such compensation in excess of one million dollars was non-deductible except to the extent the compensation was performance-based. The TCJA eliminated the exception so that all senior executive compensation above one million dollars is now non-deductible regardless of whether it is performance-based or not. This reform provides a natural experiment to study the role of tax law in influencing managerial pay decisions, an issue that has been debated for decades by scholars and policymakers. Did the elimination of the performance-based pay exception influence senior executive compensation decisions? Using a novel empirical design, we find no evidence that the repeal of the performance-based pay exception changed the most significant and salient compensation features, namely the proportion of performance-based pay to total pay and the overall amount of pay. On the other hand, when we move from headline compensation features to smaller technical ones, our data suggests that the tax change has had a significant influence. This suggests that tax rules may be only consequential in shaping executive compensation when no one else is paying attention otherwise.

Read MoreConventional wisdom suggests that the promise of tax legislation played an important and positive role in the 25% increase in the stock market that began on November 9, 2016 and continued through December 22, 2017 (the day TCJA was signed into law). Our comprehensive and exhaustive forensic analysis confirms its positive effect. With that said, we find that its net impact is relatively modest. To come to this conclusion, we first construct a novel daily human-based attribution by carefully reading the news on each of the 283 days. This exercise shows the 52 days in which tax-related news was important make up less than 1% of the total observed return. We attribute large gains to tax-related news immediately after the election as well as the build-up to passage in late 2017. However, key events in the summer of 2017 decreased the prospects for tax legislation, which wiped out most of the gains that we attributed to tax policy over the full sample. This "up, down, and up again" narrative is corroborated across a wide-range of alternative approaches, including (1) a machine-driven textual analysis based on over 1,500 possible specifications, (2) a novel probability measure tied to the passage of tax legislation constructed from prediction markets, (3) the relative performance of high tax firms compared to low tax firms, (4) a daily attribution based on firm-level regressions, and (5) several macroeconomic financial indicators. The relatively modest estimated effects are consistent with the market potentially being more driven by strong global growth, changes in other policies, a weaker dollar (which coincided with a reduction in the likelihood of passage of tax legislation), and numerous below-expectations inflation prints (keeping monetary policy at bay) that fortuitously occurred over this time period.

Read MoreWe analyze the initial corporate response to the 2017 enactment of the “Tax Cuts and Jobs Act” or TCJA. TCJA changed many corporate tax provisions, including a reduction of the corporate statutory tax rate from 35 percent to 21 percent effective in 2018 and sweeping changes to the taxation of income earned abroad by U.S. corporations. Based on a sample of U.S. corporate tax returns, we find that corporations accelerated deductions into 2017 and delayed income into 2018, thereby minimizing their taxes. We estimate an income and deduction shifting tax elasticity of -0.11 and 0.08, respectively. Additionally, we study detailed tax returns of 81 large corporations to understand how those changes impacted them.

Read MoreThis paper examines earnings management around the reduction in the corporate tax rate from 35% to 21% as enacted by the ‘Tax Cuts and Jobs Act’ (TCJA) of 2017. Building on a theoretical model that considers a higher level of book-tax conformity of ‘real earnings management’ (REM) in relation to ‘accrual-based earnings management’ (AEM), we hypothesize that firms concertedly use these manipulation techniques for different purposes. Specifically, we predict and find that firms engage in REM to shift income from the high-tax period prior to the TCJA to the low-tax period after of the TCJA to realize tax benefits. In contrast, we predict and find that firms use AEM, which has a lower degree of book-tax conformity, to simultaneously increase book income. Consistent with intertemporal income shifting, we also find that these effects reverse in 2018. Overall, our results document a potential unintended consequence of the TCJA on firm behavior that should be useful to policymakers, regulators, and researchers to evaluate the largest tax reform since 1986.

Read MoreThe Tax Cuts and Jobs Act of 2017 (TCJA) introduced two major changes that may influence the structure of executive compensation: (1) reducing corporate tax rates from 35 to 21 percent and (2) eliminating the performance-based pay exception in Section 162(m). These changes provide incentives to maximize deductible compensation expense in 2017, before the TCJA goes into effect. Therefore, we predict performance-based compensation to increase more in 2017 relative to prior years. Consistent with our expectation, we find that the increase in CEO bonus and stock option compensation is significantly greater in 2017. Our difference-in-difference results are consistent with the tax rate reduction driving the bonus increase and the repeal of the performance-based exception leading to the increase in CEO stock options. The TCJA also changed the definition of covered employees to include the CFO. We find weak evidence for abnormal increases in CFO performance-based compensation. Additional analyses indicate firms facing stronger tax incentives drive our results. Overall, our findings suggest that firms’ responded to the TCJA in the period before it was effective.

Read MoreIn 2017, Congress introduced the Opportunity Zone (``OZ'') designation to promote development in distressed communities. A criticized feature of the program is that state governors select zones from many eligible tracts without meaningful scrutiny. We find that while governors are more likely to select tracts with higher distress levels and tracts on an upward economic trajectory, favoritism seems to play an important role in governor decisions. OZ designation is more likely for tracts in counties that supported the governor in the election and when executives or firms with an economic interest in the tract donated to the governor's campaign.

Read More