Sophisticated multinational corporations are becoming ever more adept at tax planning, prompting fears that skillful manipulation of tax laws is eroding the tax base in many countries. The Organisation for Economic Co-operation and Development (OECD) is particularly concerned about this development, and has undertaken a number of initiatives to address this perceived threat to the tax base. Its Base Erosion and Profit Shifting (BEPS) project, for example, requires multinational firms above a certain size threshold to disclose their country-by-country numbers on several metrics to members’ tax authorities (e.g., the number of their employees in each country).

This country-by-country reporting currently is required on a private level in many OECD member countries, including the IRS in the United States. In the European Union, some multinational banks are also required to file public reports – and many support an extension to public reporting for large multinationals as well.

In this page, we summarize what the research has found thus far on the effectiveness of both public and private country-by-country reporting. Be sure to check back often, as more and more research is added to this growing area of exploration.

Over 100 countries now require multinational corporations (MNCs) to annually disclose geographic breakdowns of their economic activities to tax authorities through country-by-country reporting (CbCR) to combat tax avoidance. We examine whether and how this mandatory private tax disclosure affects firms’ voluntary after-tax earnings forecasts. Using difference-in-differences and regression discontinuity designs to strengthen causal inference, we find MNCs are more likely to issue after-tax earnings forecasts after CbCR implementation. This effect is more pronounced for MNCs engaging in more tax avoidance prior to the policy adoption and for those experiencing an improvement in tax-related internal information quality following CbCR. Additionally, analysts' after-tax earnings forecast accuracy improves post-policy adoption, especially among firms that increase forecast issuances. We further document an increase in the precision and disaggregation of earnings forecasts, and effective tax rate forecasts post CbCR. Our findings suggest that mandatory private tax disclosure leads to improved voluntary public disclosures, generating external benefits for capital market participants.

Read More

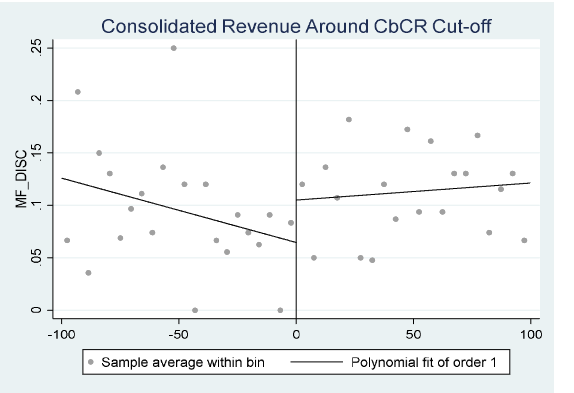

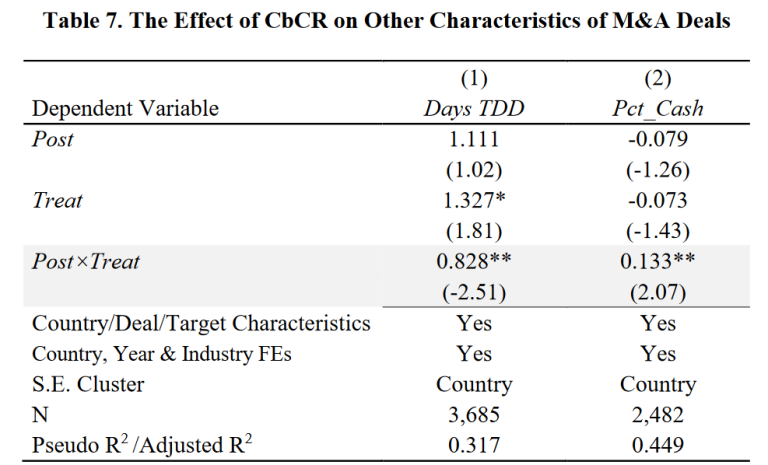

We examine the impact of mandatory private country-by-country reporting (CbCR)—a widely adopted tax transparency initiative—on mergers and acquisitions (M&As). Using difference-in-differences and regression discontinuity designs, we document a decrease in takeover premiums for affected targets in the post-CbCR adoption period relative to unaffected targets. The decrease in premiums is more pronounced for tax-aggressive targets, suggesting that acquirers price in the increased tax enforcement risk associated with these targets. More importantly, consistent with CbCR providing incremental information to acquirers and reducing information friction during the negotiation and due diligence process, we find a higher percentage of consideration paid in cash, shorter due diligence, and better post-acquisition performance for targets subject to CbCR. Our findings highlight the role of CbCR in reducing information frictions in M&As, indicating a spillover effect of mandatory private tax disclosure for a specific group of investors—M&A acquirers—beyond tax authorities.

Read More

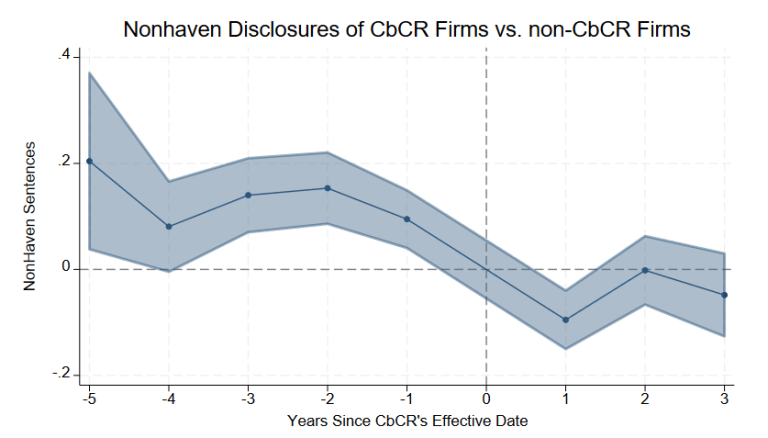

We investigate whether U.S. multinational corporations (MNCs) that are required to provide private country-level financial disclosures to foreign tax authorities subsequently change their public financial statement disclosures about foreign operations. Given differing incentives to provide information about operations in tax haven and non-tax haven countries, we separately examine changes in financial statement disclosures about operations in haven vs. non-haven countries. We also investigate whether tax audit risk moderates U.S. MNCs’ public disclosure responses to an increase in required, private disclosures to foreign tax authorities. We use the implementation of country-by-country reporting (CbCR) as our research setting and we measure public financial statement disclosures about foreign operations via text analysis tools that identify offshore words that appear in the same sentence as nation words (“foreign offshore sentences”), using Hoberg and Moon’s (2017) dictionary. We provide evidence that affected U.S. MNCs significantly reduced the number of foreign offshore sentences that appear in their financial statements after the implementation of CbCR, relative to U.S. MNCs not affected by CbCR. This reduction is driven by decreases in foreign offshore sentences about operations in non-haven countries and by firms subject to higher tax audit risk. We interpret our findings as consistent with U.S. MNCs striving to downplay the significance of operations in higher tax rate countries so that public financial statement disclosures are more closely aligned with private CbCR disclosures to foreign tax authorities.

Read More

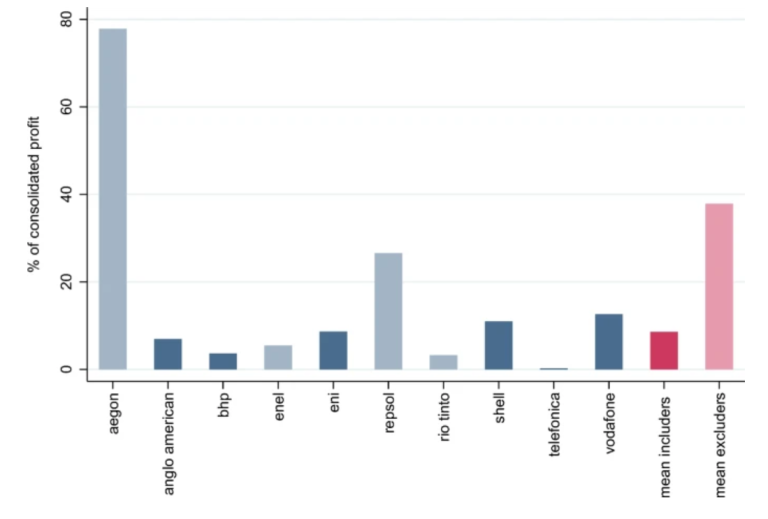

In this paper, we analyse a sample of voluntarily published country-by-country reports (CbCRs) of 35 multinational enterprises (MNEs). We assess the value added and the limitations of qualitative and quantitative information provided in the reports based on a comparison to individual MNEs’ annual financial reports and aggregate CbCR data provided by the OECD. In terms of data quality, we find that the inclusion of intra-company dividends and equity-accounted profits are a minor concern on average but that for individual MNEs corrections might be substantial. Our sample MNEs seem to pay higher effective tax rates than the global average and many of them report relatively little profit in tax havens. We only find a very weak correlation of the location of profits and effective tax rates. This might indicate that more tax transparent MNEs avoid taxes less aggressively. However, our assessment of different tax risk indicators reveals important variations between companies.

Read More

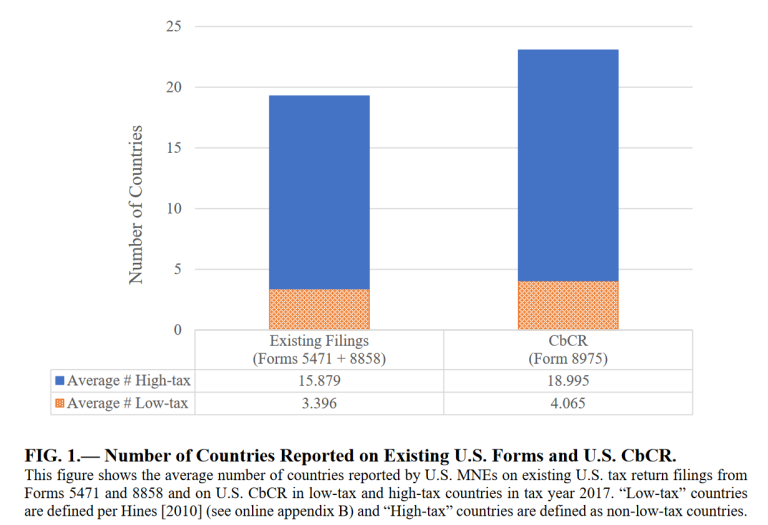

The Organization for Economic Co-operation and Development introduced country-by-country

reporting (CbCR) for multinational enterprises (MNEs) to help tax authorities combat tax-

motivated income shifting. This study uses confidential U.S. tax administrative data from 2011 to

2018 to examine the effect of U.S. CbCR adoption on the tax-motivated income shifting and real

activities of U.S. MNEs. We first document that while U.S. CbCR provides the Internal Revenue

Service with incremental information about the location of U.S. MNEs’ global activities relative to

existing U.S. tax return disclosures, we observe substantial overlap between U.S. CbCR and

existing disclosures. In contrast with prior CbCR studies in cross-country settings, we fail to find

evidence of a change in U.S. MNEs’ tax-motivated income shifting or a reallocation of real

activities based on tax incentives in response to U.S. CbCR using multiple empirical approaches.

Overall, our study leverages U.S. tax administrative data to provide insights into the impact of the

CbCR initiative on U.S. MNEs.

We examine the capital market reaction to the announcement of the European Union (EU) to introduce a public tax country-by-country reporting (CbCR) regime. By employing an event study methodology, we find a significant cumulative average abnormal return (CAAR) of -0.699%, which translates into a monetary value drop of approximately EUR 65 billion. We conclude that investors evaluate reputational risks arising from public scrutiny and competitive disadvantages to outweigh potential benefits of an extended information environment or more sustainable corporate tax strategies. In cross-sectional tests, we find that the average investor reaction is more pronounced for firms with low effective book tax rates, indicating that reputational concerns play a significant role in the marginal investor's investment behavior. Furthermore, our cross-sectional results indicate that the market reaction is stronger for firms operating in industries with high growth in market participants, providing an initial indication for the role of the competitive environment as an additional channel. Our inferences are of particular importance in light of the current ongoing debates on similar disclosure rules (particularly in the United States; cf. "Disclosure of Tax Havens and Offshoring Act") as well as for sustainability standard setters.

Read More

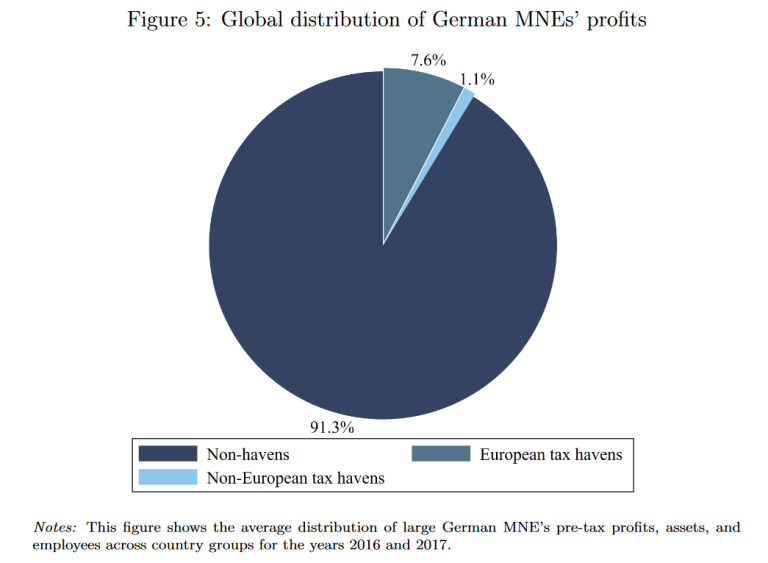

This paper is the first to use information from individual country-by-country (CbC) re-ports to assess the extent of profit shifting by multinational enterprises. Unlike other data often used to evaluate the extent of profit shifting and tax avoidance, CbC reports pro-vide a complete coverage of the global distribution of profits and indicators of economic activity for multinationals exceeding a certain revenue threshold. We show that 82% of the German multinationals subject to CbC reporting have tax haven subsidiaries and that these subsidiaries are notably more profitable than those in non-havens. However, only 9% of the global profits of German multinationals are reported in tax havens. Results from regression analysis suggest that approximately 40% of the profits reported in tax havens are a result of tax-induced profit shifting. The associated annual tax base loss for Germany amounts to EUR 5.4 billion. Adding estimates of profit shifting by multinationals not covered by the CbC data yields an overall estimate for profits shifted out of Germany to tax havens of EUR 19.1 billion per year, corresponding to 4.3% of the profits reported by these firms in Germany. This implies a tax revenue loss due to corporate profit shifting to tax havens of EUR 5.7 billion per year.

Read More

We assess the investor reaction to a potential introduction of public country-by-country reporting (CbCR) into the European Capital Requirements Directive IV. Estimating cumulative abnormal returns with the help of a multivariate regression model, we find weak significant evidence around our event date (February 20th, 2013) that investors perceive the introduction of CbCR as beneficial. In additional tests, we assess investor perceptions relative to different control groups (domestic institutions and non-EU institutions) and in the cross-section (splitting across size, systemically relevant, pre-event level of GAAP ETR and pre-event level of geographic disclosure). The only significant outcome is a negative reaction for large international EU institutions.

Read More

In this study, we examine the effect of increased tax transparency on the tax planning behavior of European banks. In 2014, the European Union introduced public country-by-country reporting requirements to the banking industry. Treating this new requirement as an exogenous shock, we find limited evidence consistent with a decline in income shifting by the banks' financial affiliates in the post-adoption period (starting from 2015). We do not, however, find robust evidence of a significant change in the consolidated book effective tax rates among the affected banks. Our findings suggest that increased transparency from public country-by-country reporting can deter tax-motivated income shifting but that it did not appear to materially influence the banks' overall tax avoidance. Our findings have policy implications for the ongoing debate between the European Parliament, the Organisation for Economic Co-operation and Development, and accounting standard-setting bodies on whether to require multinationals to publish country-by-country reports.

Read More

European regulation mandates public country-by-country reporting for banks and is expected to increase reputational costs in case of tax haven activities. We test whether the availability of additional public information on the locations of banks' subsidiaries reduces their tax haven presence. In a preliminary difference-in-difference analysis we find that indeed, tax haven presence in “Dot-Havens” has declined significantly after the introduction of mandatory public country-by-country reporting for European banks, as compared to the insurance industry which is not subject to this regulation.

Read More

We investigate the effects of mandatory private Country-by-Country (CbC) disclosure to tax authorities on economic activity. Using rich data on the operations of multinational firms, we exploit the threshold-based application of this 2016 disclosure rule in a regression discontinuity design. We find evidence that firms affected by the disclosure mandate reduce ownership in tax haven subsidiaries relative to unaffected firms and thereby increase transparency in their previously opaque organizational structure. We also document that affected firms invest less in aggregate employment on average relative to unaffected firms but do not appear to alter consolidated tax payments. However, affected firms increasingly allocate revenue, employment, total assets, and, correspondingly, tax payments to subsidiaries in European low-tax countries. Collectively, our findings suggest that mandatory CbC disclosure curbs the most aggressive tax planning achieved through tax haven operations but has likely unintended adverse effects on other real economic activities.

Read More

This paper evaluates the economic consequences of a recent global tax transparency initiative. To combat tax avoidance by multinational corporations, many jurisdictions have introduced regulations aimed at enhancing tax disclosure requirements. In particular, the Organization for Economic Cooperation and Development introduced country-by-country reporting that requires firms to provide a detailed geographic breakdown of their activity and results to tax authorities in all jurisdictions in which the firm operates.

Read More

We employ an event study methodology to investigate the stock price reaction around the day of the political decision to include a country-by-country reporting obligation for EU financial institutions.

Read More

We investigate whether mandatory public country-by-country reporting (CBCR) by European Union (EU) banks affects geographic segment reporting. We find no significant change in the reported number of geographic segments, country segments, or line items per geographic segment disclosed in segment reporting notes after the introduction of CBCR. Consistent with the notion that EU banks may aggregate geographic segments to obfuscate tax haven activities, we find a positive association between tax haven intensity and geographic segment aggregation.

Read More

We analyze the effect of mandatory financial transparency on corporate tax avoidance. Capital Requirements Directive IV by the European Commission forced multinational banks to publish key financial and tax data in the form of Country-by-Country Reporting for the first time in history.

Read More